The biotechnology industry is a booming sector with many new companies researching and developing innovative and specialized medicines. Typically, a startup biotech company will focus its limited resources on R&D and its market of origin (or some other region that’s strategically selected because of its large size and/or market potential). For a US-based company, that market is most often (unsurprisingly) the US. However, as the path to product approvability becomes clearer, global expansion plans emerge. Often, a critical early step is exploring entry into Europe.

Multiple models exist for building a European organization. However, the right model can depend on any number of factors and will vary from company to company. Each company will need to decide on an appropriate model, and customize it based on its own needs and objectives. This article outlines common models for entering Europe, as well as some key considerations regarding which model to choose based on the circumstances at hand.

Key Early Decisions

To inform an “in house” European build and navigate the geographic expansion, companies must make a range of important decisions. Most importantly, there must be alignment on the overall European vision, objectives, and strategy. Achieving this requires several early initiatives to understand the company’s full potential in Europe. For example, the company must assess the:

- Size of the European business opportunity

- Potential for market authorization

- Potential for favorable market access

- Likelihood of positive market adoption

Once the commercial assessments have been completed, it is the right time to address how the business will be designed. Developing an understanding of the people, infrastructure, and investments that are needed to capture the European opportunity will be key.

Critical questions include:

- How will the organization be built to support launches and optimize financial flows?

- What is the most appropriate country build model and how will country launches be sequenced to maximize long term value?

- What are the optimal geographic “footprint” and what countries should we enter?

Our e-book, 7 Keys to Success in Europe, as well as a collection of thought leadership resources developed collaboratively with European biotech leaders, outline a wide range of strategic considerations within these areas for any biopharma company contemplating a move into Europe.

Common Models for Europe

Once decisions have been taken and the strategy has been developed, the next order of business is to begin assessing which model to use when building countries and planning product launches. Multiple models exist for building an EU organization; however, it is important to ensure a customized model is developed for each organization.

There are several considerations companies will usually balance depending on their specific goals. For example, an ultra-rare disease company may elect to build a model that ensures EU resources are prevalent in the countries most impacted by the specific disease, whereas a company focused on a common form of cancer may build the more traditional EU HQ followed by country builds. The construct of the EU organization may also evolve over time due to organic growth factors such new product launches or new indications.

Below, we describe several of the more common models for Europe, outlining some of the pros and cons for each.

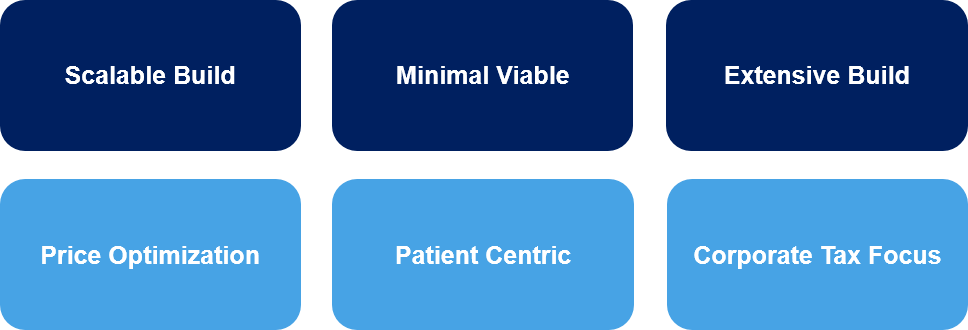

Scalable Build

This model prioritizes building a European head office as a centralized activity hub, then gradually builds up local affiliate markets with country General Managers (GMs) being based initially in the EU HQ. It often starts with few people being placed in countries and a lean EU Leadership team, then gradually scales up.

This model allows for the use of knowledgeable vendors during the leadership team recruitment period. It also ensures that the first-launch market is aligned, supported and connected to the EU HQ. Customer engagement on a local country level can be slightly compromised with this model, which is not optimal, particularly when preparing large country launches.

This model can be beneficial in certain cases. It’s often utilized prior to companies obtaining clarity from the EMA on approvability and potential launch timing. Recruitment, country builds, and operational activities are often “ring fenced” or “gated” until clarity is obtained around launch timing.

A scalable model also has applicability to all start up sizes. However, caution should be exercised if a company is less than 18 months from launch. If this model is applied late in the launch preparation process, it could result is suboptimal resourcing and have a negative impact on launch preparations, timelines, and effectiveness.

Minimal Viable

When using the minimal viable model, a company adopts a lean structure—sometimes virtual—and co-locates it with the corporate HQ, usually in the US. This uses an existing US team with vendors to support the EU build. There is also a minimal viable model where no EU HQ is built, and all EU leadership team (LT) members are in country hubs.

This option may benefit from short-term cost savings. However, several significant issues arise including poor customer/ regional engagements, significant resource constraints, excessive use of vendor support, and challenges recruiting strong talent with European insights. Given the complexity of the pricing and access environment, it is highly advisable to recruit talent who understand how to successfully navigate European markets, most of whom are based in Europe.

Extensive Build

This model establishes a European HQ and local market licenses in all core and potential revenue generating markets to ensure patient and customer needs are meet. There is also an option where the EU is built with an equivalent structure to the home market to retain consistency from the initial business build. These options are seen more commonly in companies where the first product launch will occur in Europe. However, an extensive build in Europe could be considered excessive for early launch companies, as significantly more cost-effective options are available that enable a scale-up over time and avoid unnecessary duplication of resources.

Price Optimization

The price optimization approach focuses on first-launch markets being selected with a consideration for international reference pricing implications. This approach enables sustained price preservation, speed to critical markets, potential for cluster launches, allocation of resources over time, and the sharing of “lessons learned” from several countries prior to the second wave of countries launching.

To maximize the potential of this model, companies should start planning the country launch sequencing well in advance, optimally around 18-24 months before the first country launches. This is important for preserving mid- to long-term pricing, as almost every country in Europe uses international reference pricing (IRP). As most countries launch, they enter the “reference basket” which influences the downstream pricing across subsequent countries.

In many cases, Germany is the first EU country to launch because reimbursement is automatic for EMA approved drugs, and a one-year free pricing period is granted while negotiations are underway. With the upcoming national elections in September 2021, debates are ongoing regarding changes in the insurance system, update of the AMNOG process, and other topics.

Launches in Austria, Switzerland (pending Swissmedic approval), and the Nordic region frequently coincide with the launch in Germany due to the relatively high pricing levels and a general ease and effectiveness of negotiations. These countries are often considered as the first-wave launch markets.

Second-wave launch markets often include France and Italy with the third wave usually including the UK and Spain These two countries are often in a later wave of launches (2+ years after the first wave markets), as reimbursement is dependent on the outcome of cost effectiveness assessments (UK) and lengthy negotiation with national, regional and local decision makers (Spain).

The price optimization model is the most frequently used market entry model for specialty care companies.

Patient Centric

This model leverages a very small European HQ with most team members being in countries where the largest patient populations exist. This decentralized approach has been used in ultra-rare, usually genetic diseases where the epicenter of patients may be within 2-3 smaller countries and allows for greater customer engagement. Due to the small numbers of patients, organizational builds are usually more streamlined, requiring smart and efficient use of resources. The utilization of unconventional skills and knowledge may also be required with this model. For more information on the concept of patient centricity, please take a look at patient centricity case study 1 and case study 2.

Corporate Tax Focused

This is viable for companies aiming to maximize the long-term tax benefits with IP/relevant teams located in a low-tax country. It remains attractive usually with larger corporations. Companies have traditionally focused on placing their HQs in regions that offer financial benefits, such as Switzerland and Ireland. However, with continuously changing taxation systems across the US and Europe, this model needs to be re-assessed frequently.

Blended Options

While there are several operating models to choose from, it is common for companies to select a “blended option” allowing for the benefits of several selections and, at times, negating risks. For example:

- Building Europe with the goal of optimizing price potential over the longest period, while enabling high volumes of patients to access treatments. Price optimization is often achieved by recruiting specialist market access and health economics team members. In addition to local thought leader engagement, significant time is spent with payers and health technology customers to understand local market needs and deliver high quality submissions. Near parallel resourcing is also required across multiple first-launch countries which can be a heavy lift for the EU HQ team. Initial launches are in Austria, Germany, some Nordic markets and potentially Switzerland, followed by France and Italy. Spain and the UK are generally wave two or three launch markets due to their internal pricing and access controls. In this scenario price optimization is usually achieved while ensuring the largest numbers of patients benefit from treatments.

- Building a very small European HQ, extensively leveraging vendors and recruiting a team over time; Optimizing IP/tax opportunities by locating in Switzerland. The location will enable the company to leverage the taxation benefits, a strong international talent pool and readily available vendors. Head count and country builds are “gated” until there is greater certainty of approval and market access. Leveraging the vendor population in Switzerland also enables the company to scale over time.

- Early recruitment of a General Manager of Europe based in the corporate HQ to assist with clinical and access requirements in phase II. The GM locates in the EU HQ to commence the organizational build between 24-30 months prior to launch. Significant hiring, particularly in the countries, should be gated until a positive readout of Phase III data, followed by a full-scale build.

Parting Thought

In general, there are multiple options companies can select from to build their European organizations. However, in all options there is one constant is that it is strongly advised: hire a very solid and experienced General Manager of Europe, and don’t wait too long to do so. The GM should be on board early enough to assess the company, understand the market situation, and tailor the launch model to optimize the company’s potential for success.

The Authors:

Theofanis Manolikas – Principal & Pathfinder Lead, Blue Matter

Theofanis Manolikas – Principal & Pathfinder Lead, Blue Matter

Michelle Lock – SVP, Head of Europe & International, Acceleron

Michelle Lock – SVP, Head of Europe & International, Acceleron