The global contract development and manufacturing organization (CDMO) market for biopharmaceuticals has been experiencing an influx of private equity (PE) firm interest for several years. This has been driven by rising demand for complex therapeutics, policy tailwinds, and the cost effectiveness of outsourcing. Growth trends across the CDMO value chain and modalities are presenting new opportunities for promising, long-term investments. In this article, we review the key dynamics shaping the market and offer a playbook investors can use to realize growth opportunities.

Background

CDMOs serve as the outsourced development and manufacturing backbone of the pharmaceutical industry, enabling pharma and biotech companies to efficiently develop, scale, and commercialize novel biopharmaceutical products, from early clinical batches (preclinical through Ph 2) through large-scale commercial production (Ph 3 and beyond). By outsourcing to CDMOs, companies gain flexible access to specialized expertise, advanced infrastructure, and scalable capacity without the capital intensity and operational complexity of building these capabilities in-house.

Market Overview

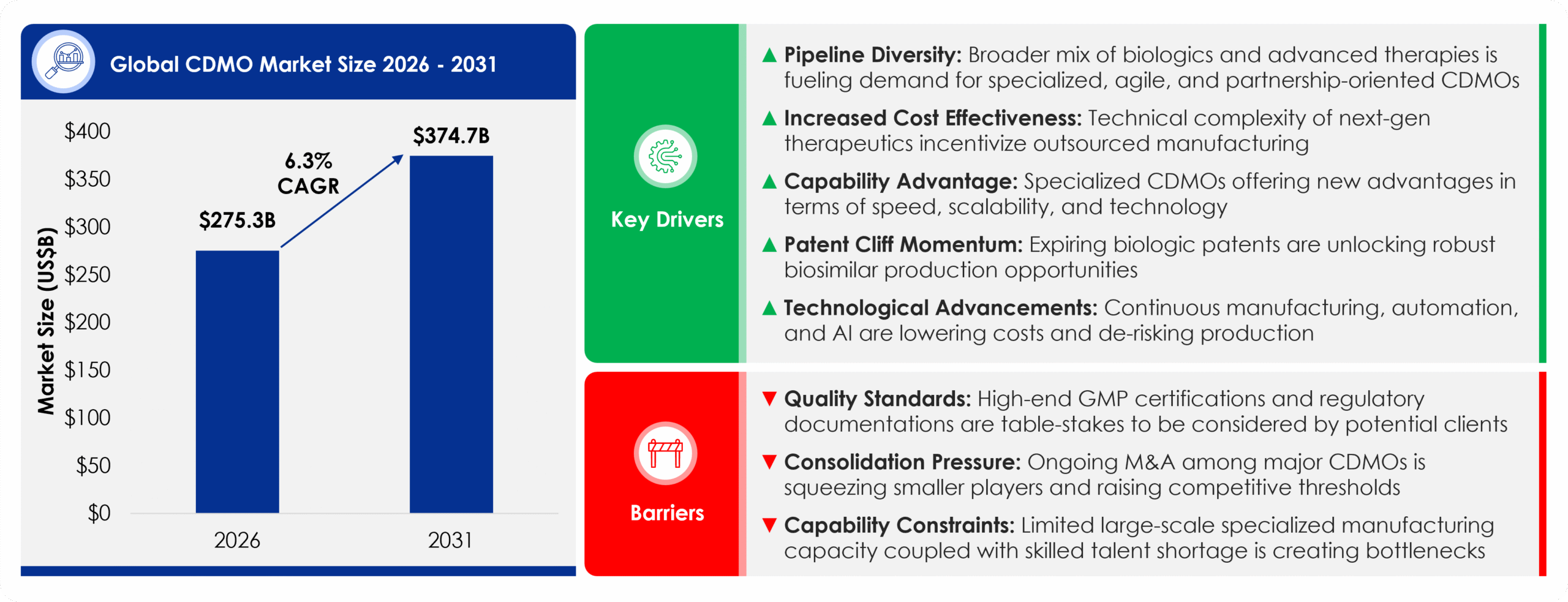

Figure 1: CDMO Market Snapshot

The biopharmaceutical CDMO market has experienced some volatility in recent years. Demand surged in 2020-2021 during COVID and then normalized in 2022. This correction mirrored broader biopharma market dynamics. Looking ahead, the global CDMO market is expected to grow from ~$275 billion in 2026 to ~$375 billion by 2031, representing a ~6.3% compound annual growth rate (CAGR)[1].

The combination of a fragmented market coupled with strong and reliable underlying demand makes CDMOs a highly attractive segment for PE investors. PE–backed transactions have consistently accounted for a majority of CDMO M&A activities over the past several years.

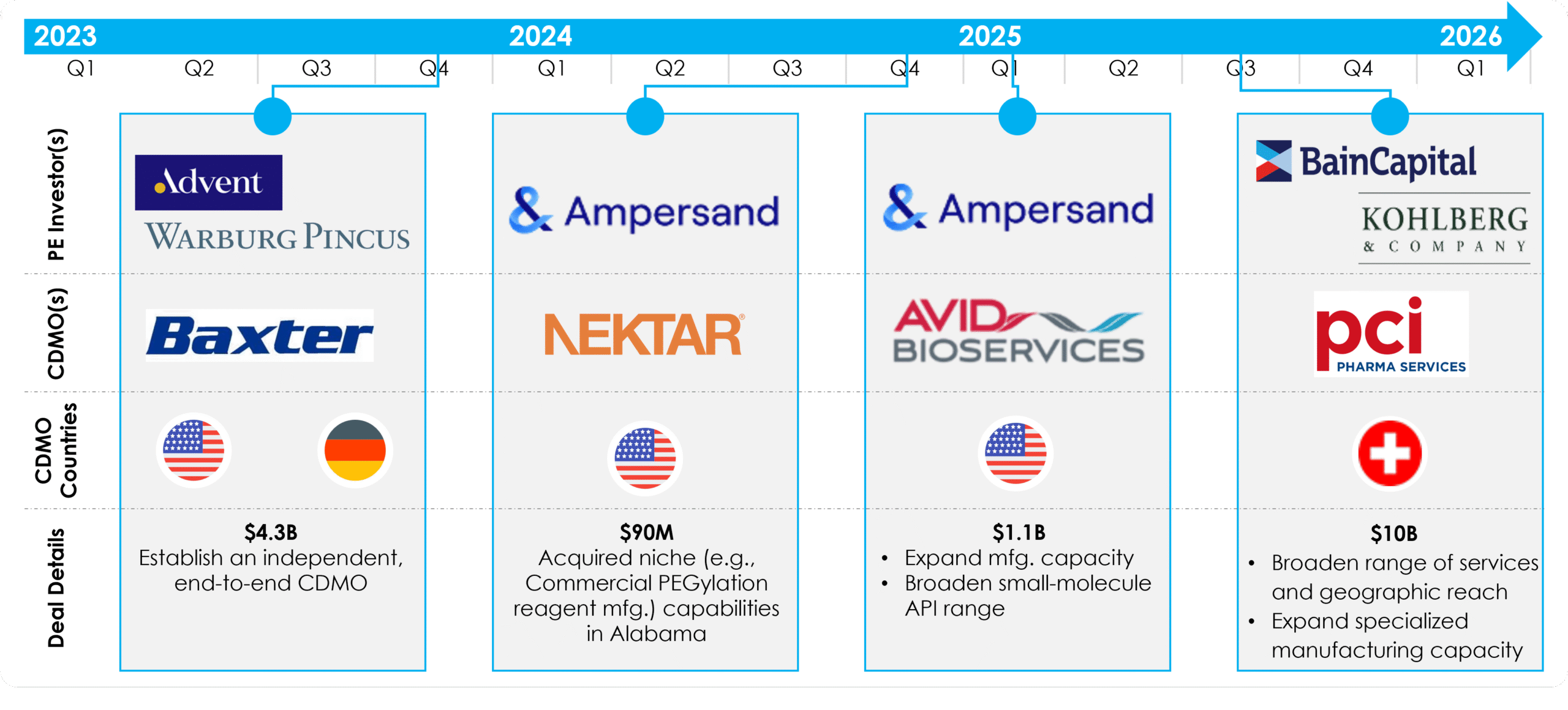

Recent transactions collectively illustrate signals of investor conviction in CDMOs as durable, high-value assets, particularly in the United States.

Figure 2: Recent CDMO Transactions

Opportunities and Risks for PE Biopharma CDMO Investors

From a PE perspective, biopharma CDMOs represent a compelling yet nuanced opportunity. Structural drivers underpin recurring revenue streams and platform growth potential. At the same time, investors must rigorously assess operational and market risks that can materially impact ROIC and exit value. The following section synthesizes key opportunities alongside critical risks for PE investors to consider.

Opportunities

Inherent Biopharma Partnership Dynamics

CDMOs derive long-term value from their strategic relationships with biopharma clients. Demand for their services is largely non-cyclical and resilient through macroeconomic cycles, with revenue often backed by multi-year supply agreements tied to essential medicines. High switching costs, regulatory hurdles, and deep client integration create stable, predictable cash flows. Increasingly, CDMOs are moving from commoditized service providers to strategic partners, offering value-added capabilities such as process optimization, rapid scale-up, regulatory support, and integrated development services that accelerate clients’ time-to-market.

Biopharma Outsourcing Incentives

Outsourcing is becoming increasingly cost-effective for biopharma customers as it enables them to streamline development / manufacturing costs across diverse and complex pipelines. This is particularly important today as next-generation biopharma modalities require advanced manufacturing capabilities that are expensive and time-consuming to build in house (e.g., ADCs, bi/multi-specifics, peptides, complex biologics):

- ADCs (Antibody-Drug Conjugates): The global ADC contract manufacturing market is expected to grow from ~$9B in 2024 to ~ $17B by 2030 at an 11% CAGR[2] due to the rising cancer burden and complex manufacturing. Unique manufacturing capabilities are required to meet ADC demand, including high-potency payload handling, conjugation chemistry, combined biologics/small-molecule purification, advanced analytics for heterogeneity/stability, and sterile fill-finish via aseptic processing.

- Bi-/multispecific Antibodies: Bi and multispecific antibodies are projected to grow from ~$2B in 2025 to ~$6B in 2035 given the growing demand, particularly in oncology and immunology[3]. Manufacturing bi/multispecifics requires complex cell-line and expression strategies, complex downstream separation and purification, highly specialized characterization of binding/functional properties, and robust regulatory documentation.

- GLP-1 / Peptide Therapeutics: The global peptide CDMO market is predicted to grow at a ~16% CAGR from ~$4B in 2025 to ~$11B in 2032 due to the rapid expansion of metabolic, obesity and cardiovascular indications for GLP-1 analogs and peptides[4]. These molecules, especially injectable GLP-1’s require large-scale complex capabilities including peptide synthesis/purification, formulation of long-acting products, sterile/aseptic fill-finish, and high throughput scale-up.

- Complex Biologics: Given the rising demand for complex biologics / biosimilars, the global biologics CDMO market size is expected to grow from ~$19B USD in 2024 to ~$43B in 2033 at a CAGR of ~9.2%[5]. CDMOs that support these modalities need specialized processes, advanced analytical characterization, modality-specific manufacturing platforms, and rigorous quality and regulatory expertise to reliably deliver at commercial scale.

- Additional Advanced Modalities: Beyond the above, there are other biologics/advanced therapy modalities with their own unique manufacturing requirements, including mRNA/siRNA therapeutics, radionuclide conjugates, and other precision platforms, that will contribute to the demand for CDMOs.

Technological Advances Driving Operational Efficiencies

In parallel, new technologies in continuous manufacturing and digital / AI-driven platforms are reducing the costs and risks associated with molecule development and manufacturing. Continuous manufacturing drives faster throughput, lower waste, and real-time quality control. An FDA audit found continuous production gets products to market ~12 months sooner than batch processes[6]. Meanwhile, AI-driven platforms, digital twins, predictive analytics, and automated QC are streamlining operations and reducing risk.

Policy Tailwinds Opening New Opportunities

For decades, the pharmaceutical industry relied on low-cost offshore production, particularly in China and India. Now, there is rising pressure to reshore drug production and secure fragile supply chains as governments and investors respond to shortages, geopolitical risk, and patient demand. US-China pharmaceutical-import tariff threats are pushing drugmakers to locate API and sterile manufacturing capacity in North America or the EU rather than rely on overseas suppliers. The culmination of these policy tailwinds opens new opportunities for US and European CDMOs by reshoring from India and China. According to a Black Book Research survey of 78 venture capital, PE, investment banking, and healthcare technology influencer respondents, supply chain resilience is a top priority, with nearly half of survey respondents saying CDMOs with active U.S. or EU reshoring strategies were “significantly more attractive” for capital allocation.[7]

Market Fragmentation

The biopharma CDMO market remains highly fragmented, which continues to be a driver of PE interest. This fragmentation creates a large white-space opportunity for consolidation, enabling PE investors to roll up multiple smaller CDMOs to build organizations with broader service offerings and the operational efficiencies that come with economies of scale (e.g., combined overhead, compliance, infrastructure). As demand for outsourcing continues to grow, these roll-up strategies remain attractive for capturing market share and exit-able platforms.

Risks

High Barriers to Entry

Building a competitive CDMO requires substantial capital investment, specialized workforce expertise, regulatory certifications, and a global quality infrastructure. For advanced biologics and high-potency molecules, lead times for facility build-outs or retrofits can exceed 3–5 years.[8] These structural barriers—coupled with the “stickiness” of network driven market dynamics—reinforce incumbents’ advantages and support attractive long-term industry economics.

War on Talent

The “war on talent” represents a critical operational risk for PE investors in biopharma CDMOs, as the industry increasingly relies on highly specialized, GMP-trained personnel to support complex biologics, cell and gene therapies, and advanced modalities. Shortages of process engineers, viral-vector specialists, and quality assurance professionals are widespread, and turnover is high, undermining operational stability and project timelines. Moreover, competition for talent drives wage inflation and increases operational costs, potentially compressing margins. As a result, workforce scarcity could materially impact the profitability and exit potential of PE investments in CDMOs.

Uncertain Long-term Global Dynamics and Sponsor Demands

PE investors in biopharma CDMOs face significant uncertainty from global macroeconomics, supply chain, and pricing pressures. Regulatory shifts, geopolitical tensions, raw-material shortages, and trade restrictions can disrupt operations, increase costs, or delay projects. At the same time, rising pressure from payers and governments to lower drug prices fuels demand for cheaper manufacturing solutions creating potential revenue and margin risk.

Tech-transfer complexity and modality inflexibility

Another structural risk in CDMOs is the complexity of tech transfers and the inflexibility of specialized manufacturing facilities. Advanced therapies such as cell-and-gene therapy, antibody-drug conjugates, or viral-vector biologics require highly bespoke manufacturing processes. Facilities built for one modality may not be repurposed for others, meaning that a downturn in demand for a specific modality could leave expensive infrastructure idle. For PE investors, this reduces asset fungibility and increases operational risk, as the expected returns are contingent not only on capacity but also on the ability to execute complex tech transfers efficiently.

Investor Strategy

Building on these considerations, PE investors may leverage this framework to systematically evaluate where their capital can generate the most value while managing exposure to operational and market risks.

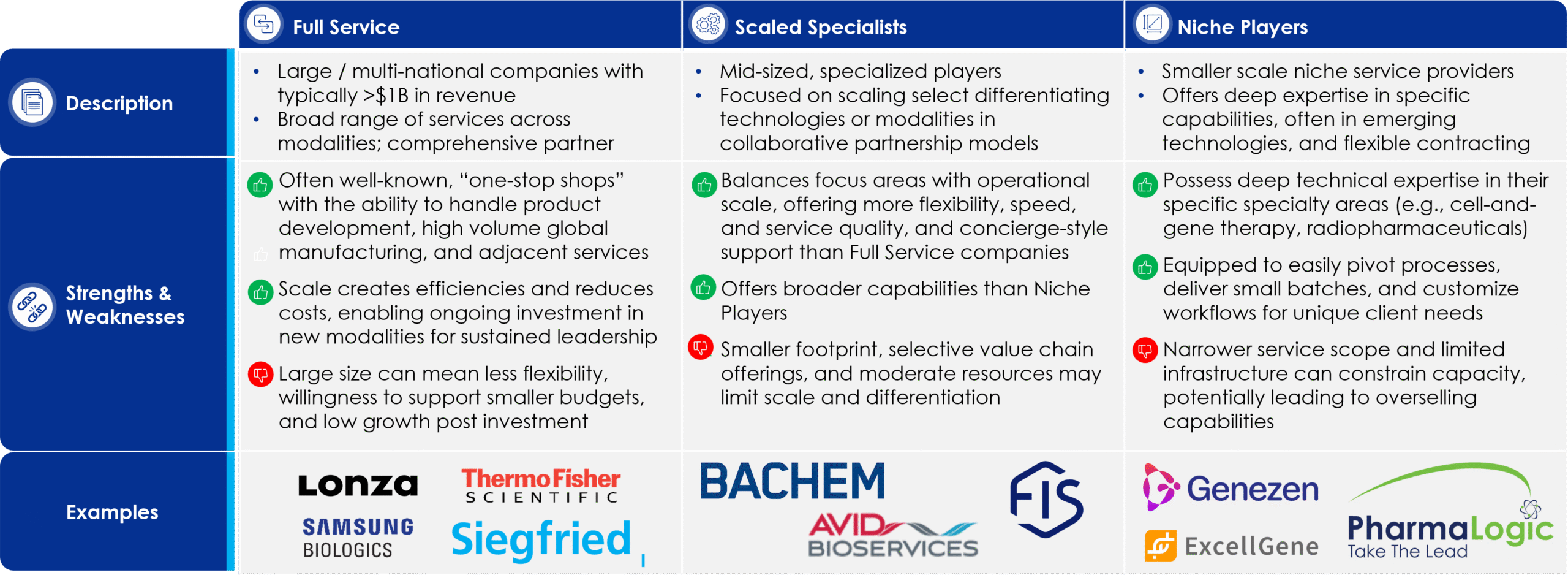

Across the landscape, three primary CDMO archetypes emerge based on revenue scale, service breadth, and strategic positioning: Full Service, Scaled Specialists, and Niche Players. Full Service companies, such as Lonza and Samsung Biologics, provide end-to-end capabilities and broad platform coverage, benefiting from economies of scale but sometimes can sacrifice agility and customization. They can appeal to investors prioritizing stability and lower risk investments, albeit with likely more modest upside. Scaled Specialists occupy a middle ground, combining targeted expertise with sufficient breadth to serve a diverse client base, making them attractive for investors seeking scalable platforms with both organic and inorganic growth potential. Niche Players, by contrast, offer deep technical specialization and greater flexibility, often in emerging modalities or niche capabilities creating defensible positioning, but can be constrained by throughput and infrastructure.

Figure 3: Three Primary CDMO Archetypes

Once investors determine which CDMO archetype best aligns with their risk tolerance and value-creation strategy, the next step is to drill deeper through targeted segmentation to identify growth opportunities across the value chain. A segmentation-first investment thesis enables PE firms to pinpoint CDMOs whose service mix, modality focus, technology maturity, and geographic footprint align with areas of unmet need or accelerating demand. Importantly, segmentation must be tailored to the investor’s strategic objective. For example, a platform seeking to expand into new dosage forms may segment by product type, while a firm pursuing business-model diversification may map the landscape by geography, service line, or modality. In this way, investors can not only choose where to play at the archetype level, but also how to win by identifying capability gaps, growth pockets, and underpenetrated segments that offer the strongest potential for value creation.

As PE firms evaluate CDMO opportunities, investors may adopt a forward-looking approach by assessing how well potential CDMO targets are positioned against biopharma’s evolving preclinical and clinical pipelines. CDMOs that have already built, or are strategically developing capabilities in high-growth, complex modalities such as ADCs, bispecifics, or GLP-1s are generally better placed to compete for future demand and may benefit from premium pricing driven by capability scarcity. Monitoring pipeline trends can help investors align capacity and capability investments with areas where sponsor demand is likely to accelerate.

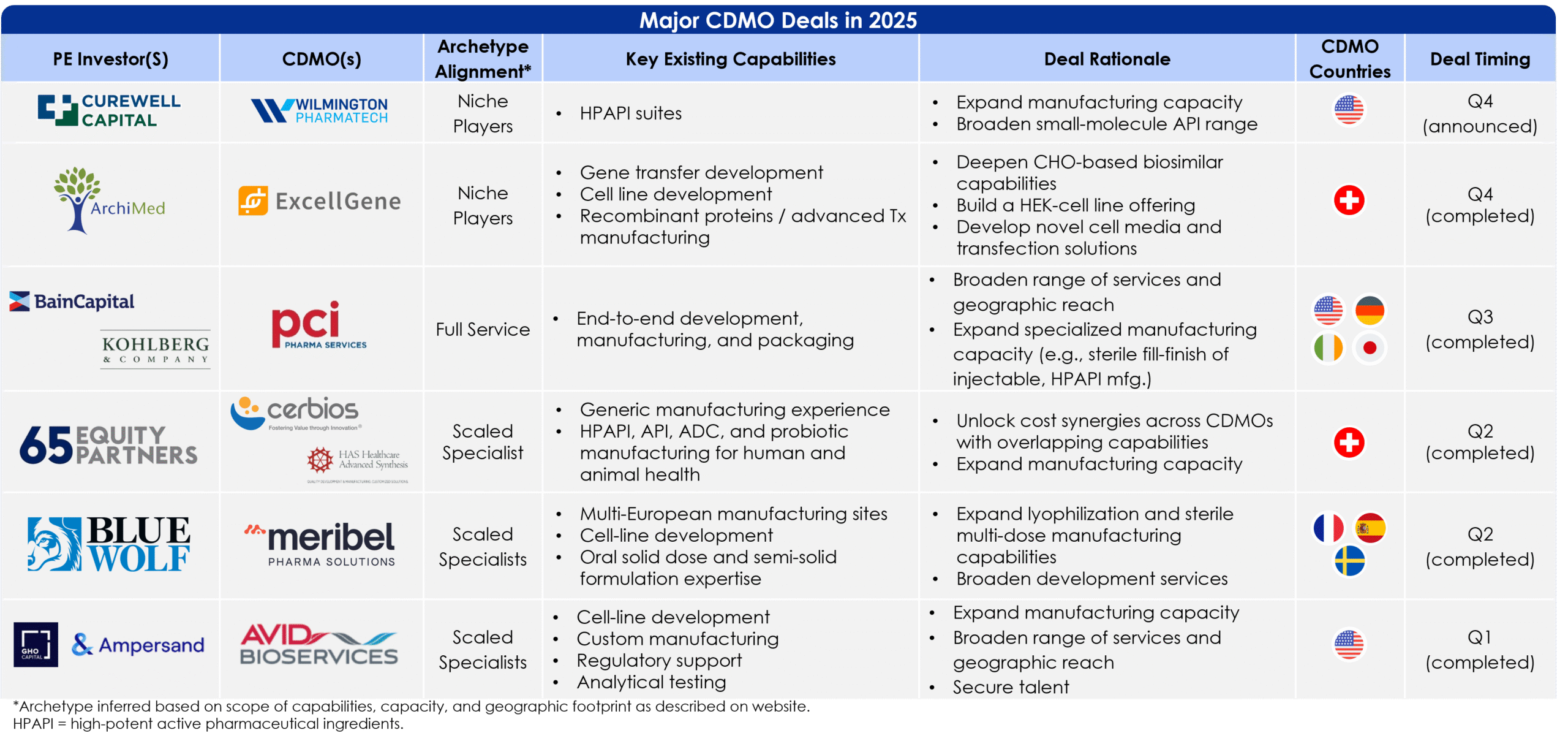

Recent deals in 2025 highlight these trends:

Figure 4: Major CDMO Deals, 2025

Across these recent CDMO transactions, deal rationale is not one-size-fits-all but instead maps to each company’s archetype. Full Service companies like PCI attract investors looking to scale proven, in-demand capabilities (e.g., sterile-fill and packaging platforms) and consolidate fragmented capacity from competitor CDMOs. Scaled Specialists, such as Cerbios and Meribel are developing their range of capabilities to capture rising demand. Meanwhile, Niche Players like ExcellGene and Wilmington Pharmatech are investing in highly technical, upstream biologics enablers where proprietary know-how, cell-line development expertise, or niche modalities create defensible positioning and strong pull-through from the emerging pipeline. Across all three archetypes, the most attractive CDMOs are those whose differentiated capabilities directly map to pharma’s future needs.

Conclusion

The biopharma CDMO sector offers compelling opportunities, but success requires a nuanced, disciplined approach. Investors who align to the right archetype, anticipate future customer demands through pipeline insights, and build or acquire the right capabilities are best positioned to capture durable growth. In a market defined by complexity, specialization, and consolidation, strategic clarity combined with operational excellence will separate high-performing platforms from the rest.

Endnotes:

[1] Mordor Intelligence. Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market Size, Share & Companies 2026-2031, Jan. 2026

[2] Grand View Research. Antibody Drug Conjugates Contract Manufacturing Market Report 2025–2030. Grand View Research, Nov. 2025

[3] BIS Research. Bispecific and Multispecific Antibodies Market – A Global and Regional Analysis: Focus on Molecular Format, Application, Mechanism of Action, End User, and Regional Analysis, 2025–2035. Nov. 2025

[4] Intel Market Research. (2025). Global Peptide CDMO Market Outlook 2025-2032. Intel Market Research. Jul. 2025

[5] Grand View Research. Biologics Contract Development And Manufacturing Organization (CDMO) Market Report, 2025–2033. Grand View Research. 2025

[6] Health Sciences Forum. “Continuous Manufacturing and CDMOs: A New Era in Drug Production.” Health Sciences Forum. Jul. 2025

[7] Yahoo Finance. Pharma Contract Manufacturing is the Quiet Reshoring Engine Investors Can’t Ignore. Sept. 2025

[8] CDMO World. Biologics CDMO Transition to Commercial Scale: A Guide. 2024. CDMO World blog/page