One year ago when we published an in-depth review of the cell-based immunotherapy landscape, no one could have predicted the global COVID-19 pandemic and its associated disruptions. But researchers, drug developers, regulatory agencies, clinicians, and patients all worked hard to ensure that the cell therapy field continued to advance and deliver promising new treatments in oncology. Notably, many of the pre-2020 top-of-mind key questions about both commercial success and scientific potential have now been answered – some of them in surprising ways.

Here, we will:

- Briefly align on the core design elements and open questions surrounding cell-based therapies in oncology:

- Overview: What has changed for cell therapies in 2020?

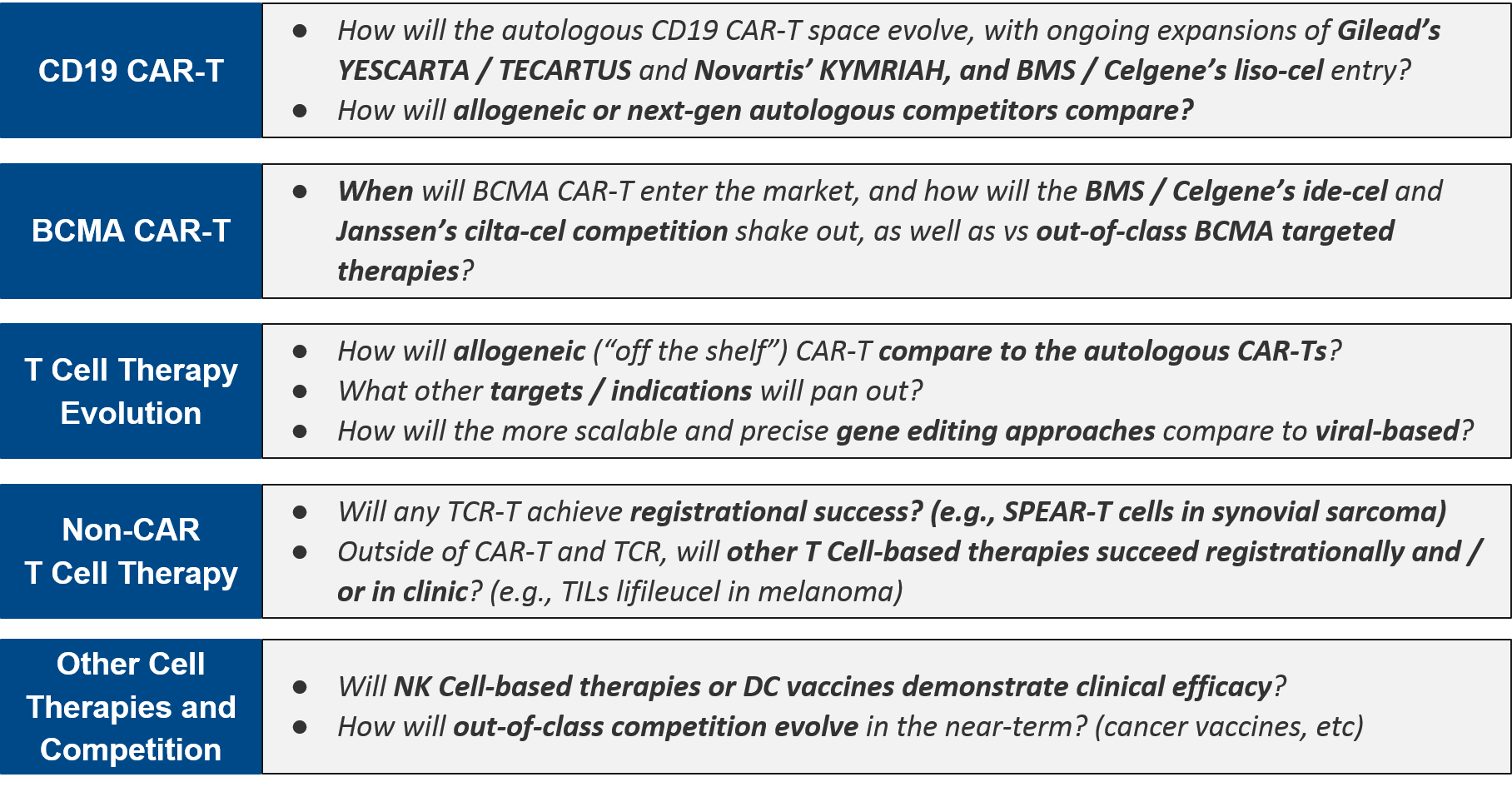

- CD19 CAR-Ts: Competition heats up between the autologous players – can allogeneic and next-gen designs displace?

- BCMA CAR-Ts: which (class of) therapy will take the prize in multiple myeloma?

- What’s Next for CAR-T Cell Therapies: Other targets, technology advances, solid tumors?

- Non-CAR-T Cell Therapy (TCR-T, TILs, etc) – will we see approval(s) in 2021-22?

- Other Cell Therapies: (When) will NK Cells and new DC Vaccines succeed in clinic?

- Review major research, regulatory, and commercial progress during 2020 that has addressed or begun to address these key questions

- Outline the key milestones for 2021-22 that will further address these questions

Overview: What has changed for cell therapies in 2020?

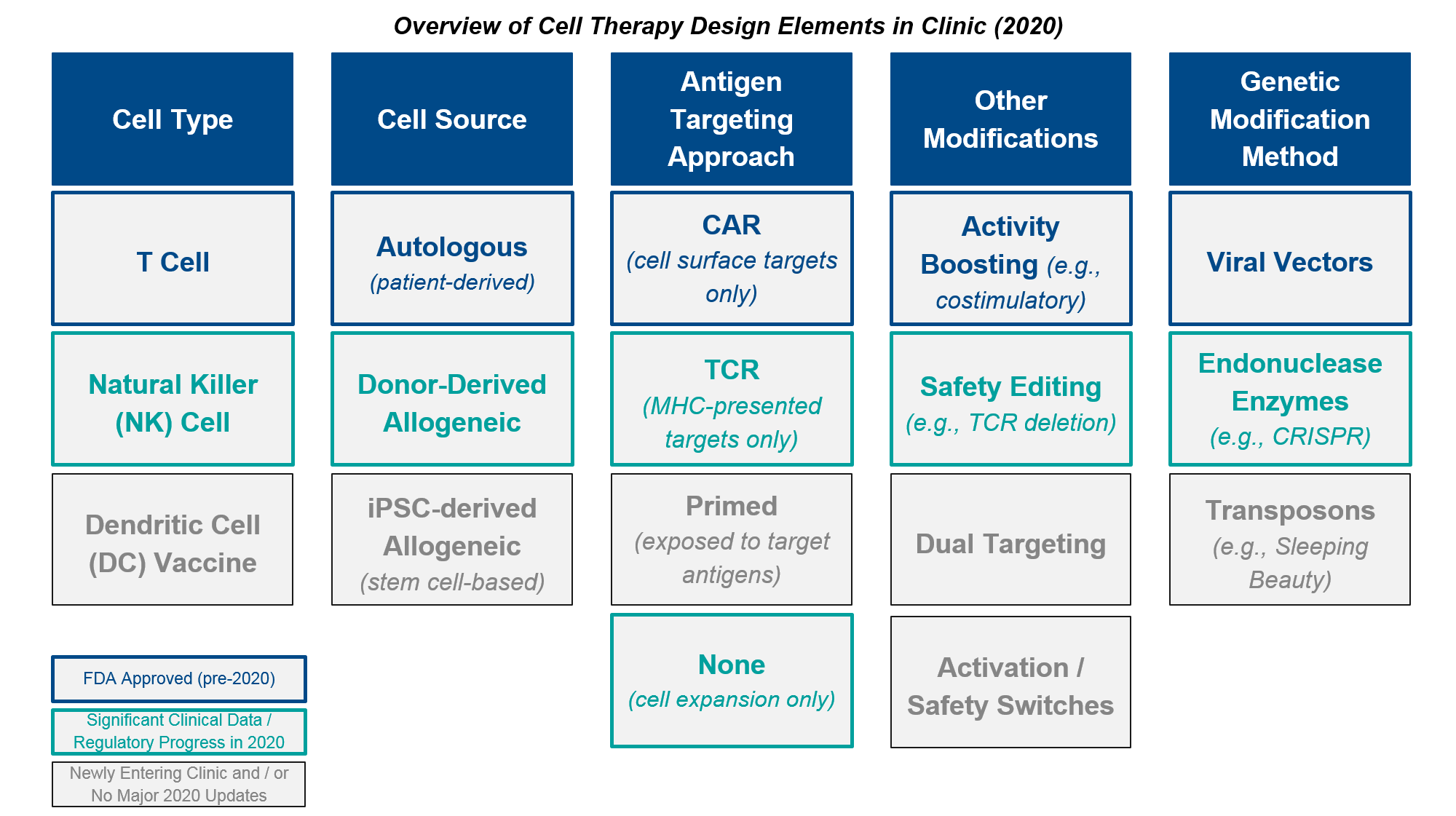

Cell therapy design requires selection(s) from each column of the elements above, chosen to complement and supplement each other’s attributes. In addition, cell therapy development programs must also define the target (where relevant) and indication(s) for clinical trials. For a deeper dive on these elements and associated design considerations, please see our previous report here.

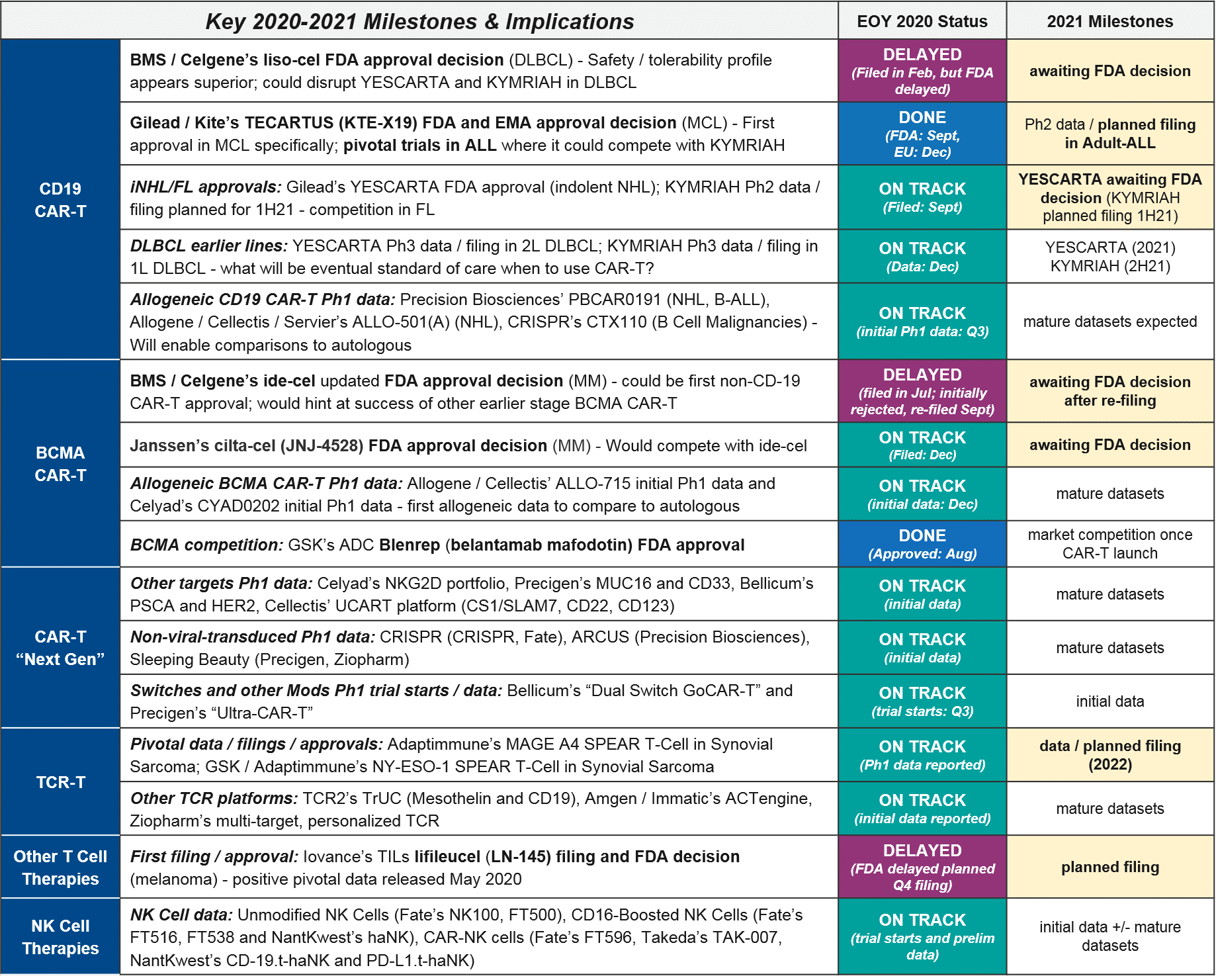

In addition to various clinical and regulatory developments regarding these design decisions and attributes (discussed further below), 2020 also brought a major external disruption to cell therapy development and commercialization, namely, the COVID-19 pandemic and its associated crises. In addition to the incalculable impacts of COVID-19 on individual cancer patients and health care providers, the pandemic also impacted several anticipated 2020 milestones across the cell therapy landscape. Most notably, the FDA cited COVID-19 as a reason for manufacturing inspection delays that made liso-cel miss its end of year approval target, therefore losing out on a major milestone payout. In addition, various clinical trials experienced pauses and delays in enrollment, which will no doubt impact data release timelines in the future.

At the beginning of 2021, the cell therapy market is dominated by Novartis’ KYMRIAH and Gilead’s YESCARTA and TECARTUS which share many design commonalities. They have the same CD19 target and despite different order of approvals they now have overlapping indications in leukemia/lymphoma, and they are all autologous, costimulatory-boosted CAR-T cells generated using viral vectors. While we can now rest assured that these particular design elements have proven efficacy and a well-understood safety / tolerability profile, there is always room for improvement in the overall product profile. This includes efficacy, safety, and—crucially for these complex therapies—speed and ease of manufacturing and delivery to the patient. Separately, there is enormous opportunity if cell therapies can succeed in other targets and indications. This extends beyond BCMA in multiple myeloma (where we expect one or more CAR-Ts to be approved in 2021), perhaps to include solid tumors too, where the TCR-Ts and TILs could be approved within 2021-2022.

Several of these design decisions / possible improvements from the established autologous CAR-T design are at the forefront lately, particularly the question of autologous vs allogeneic cell source. Autologous CAR-T manufacturing is inherently time-consuming and expensive, as it requires T cells to be successfully obtained from each individual patient, then purified, modified, expanded, and infused back into the patient.

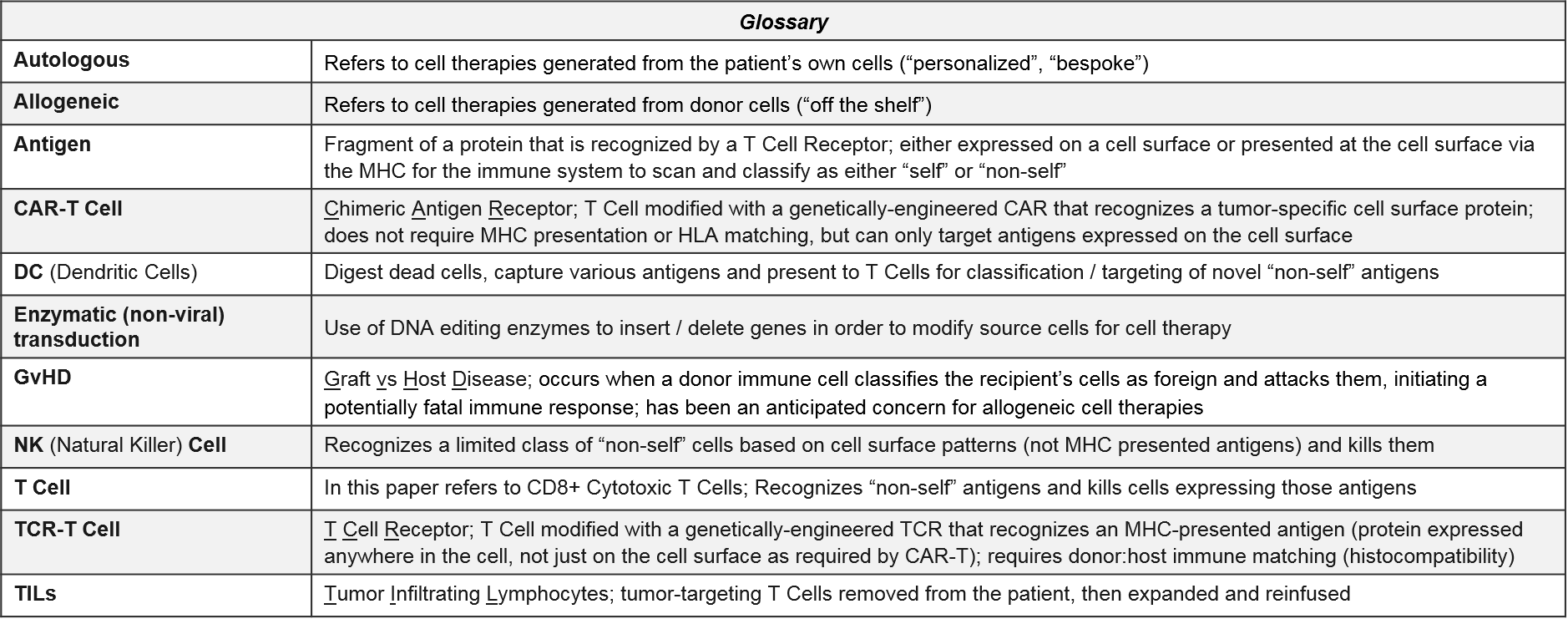

Allogeneic CAR-T manufacturing, on the other hand, begins with source cells from a donor or iPSC (induced-pluripotent stem cell)-generated pool, and can therefore skip ahead to the modification step. While faster and cheaper to produce, it has been unclear whether these cells would be as efficacious as patient-derived ones. There are also concerns about donor vs host immune reactions, e.g., Graft vs Host Disease (GvHD). Below, we will review emerging data that suggests possibly comparable efficacy as well as an encouraging lack of GvHD. Based on these data, it seems quite possible that the allogeneic platforms will succeed as both safe (i.e., no GvHD or any worse AE than the autologous ones) as well as effective enough to achieve registrational success. The open question is whether they will match the efficacy of the autologous; if they are somewhat less effective but much quicker and cheaper, consumers will have to make trade-off decisions.

Another big question is whether the enzymatic (non-viral) gene modification methods such as endonucleases like CRISPR or transposon-mediated approaches like Sleeping Beauty would prove functional. They offer both greater scalability as well as more precise insertions than the traditional viral transduction approaches. While these approaches are relatively new, we do have several in clinic now with early data reported in 2020. Early evidence suggests that the non-viral genetic modifications are comparable to the viral-based ones. While it is unlikely they would offer any efficacy benefit, their use would make manufacturing more precise and scalable, so if these early findings pan out we would expect rapid uptake across manufacturers.

One overarching and still open question, which involves all forms of cell therapy, is whether any cell therapy will truly succeed in solid tumors. Based on current data and announced timelines, we could see near-term approval of TILs (lifileucil) in melanoma and one or more TCR-T therapies in synovial sarcoma, which on the face of it are quite different indications (common vs rare, many treatments vs few, immunologically “hot” vs “cold”). It remains to be seen what common themes, if any, connect solid tumor indications where cell therapies achieve both regulatory and commercial success.

Overall, despite the impact of COVID-19 on clinical trials and R&D, in 2020 we saw numerous developments and hints of future promise that address these and other key questions about the future of cell therapies, as well as some unexpected regulatory setbacks.

We anticipate 2021 will be an even richer source of new data and decisions that will further characterize the ultimate potential of cell therapies, namely:

CD19 CAR-Ts: Competition heats up between the autologous players – can allogeneic and next-gen designs displace?

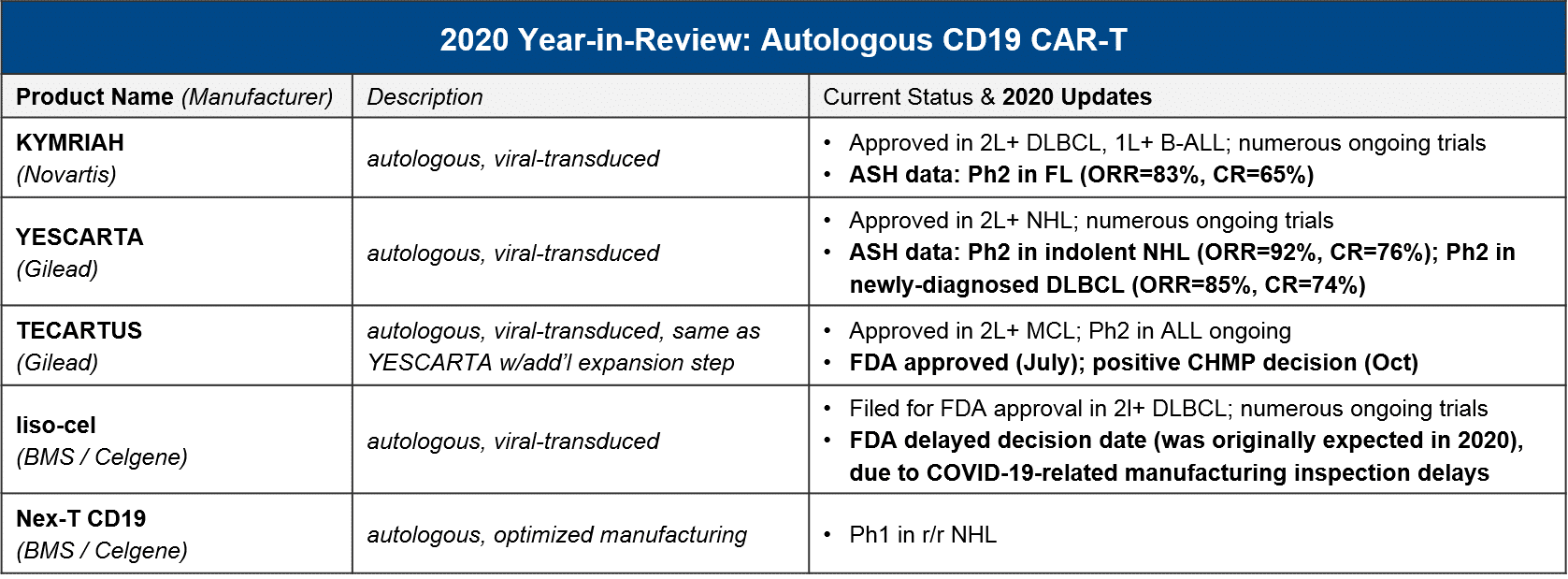

In the almost three and a half years since the first CAR-T (Novartis’ KYMRIAH) was approved, only two other CAR-T therapies have been FDA approved (Gilead’s YESCARTA just two months later, and their TECARTUS in 2020). Notably, all three of these products are autologous CD19 CAR-T with a focus in NHL and B-ALL.

At the beginning of 2020, the FDA granted a priority review for BMS / Celgene’s autologous CD19 CAR-T liso-cel, setting the expectation that it too would join them in DLBCL this year. However, in May the FDA announced it was delaying its decision until November 2020, citing COVID-19-related delays in manufacturing inspections. Further delays have pushed the decision into 2021, an unfortunate development for stockholders as the liso-cel approval by the end of 2020 was one of three milestones required for a payout. Meanwhile, both KYMRIAH and YESCARTA are pushing towards new labels in NHL. They both announced positive data in FL (iNHL) at ASH, and YESCARTA also announced positive data in newly-diagnosed DLBCL.

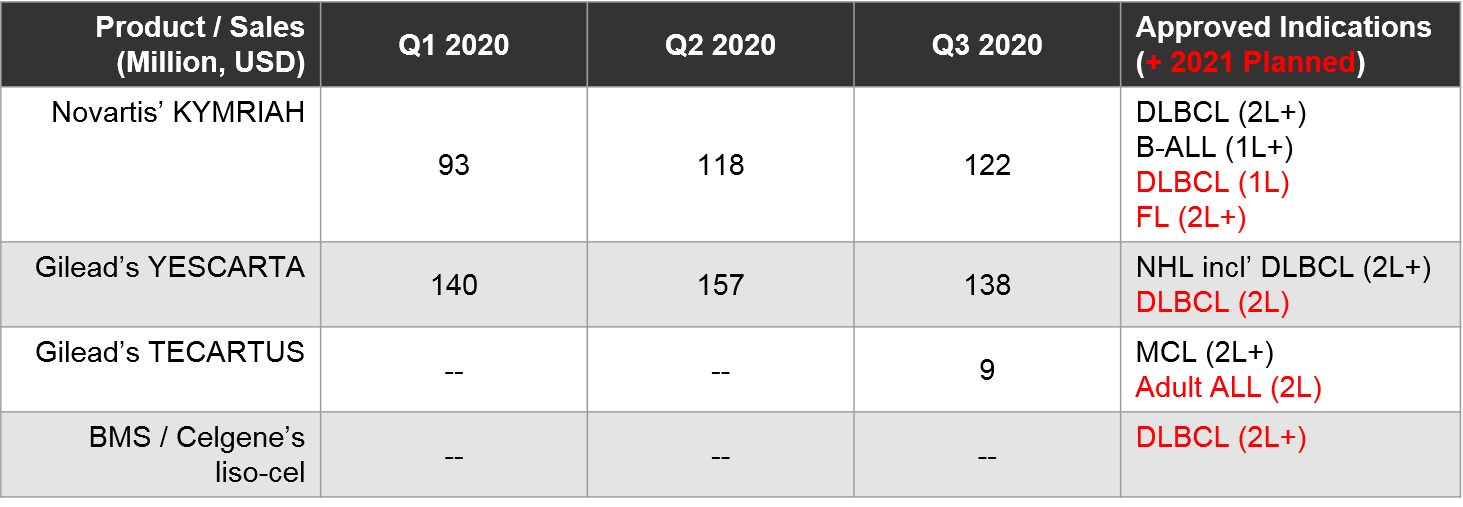

At the time of this writing, direct competition between marketed autologous CD19 CAR-T is restricted to 2L+ DLBCL, where both YESCARTA and KYMRIAH are approved. All other approved indications are non-overlapping (YESCARTA also has a broader NHL label, KYMRIAH has a B-ALL label, and TECARTUS has an MCL label).

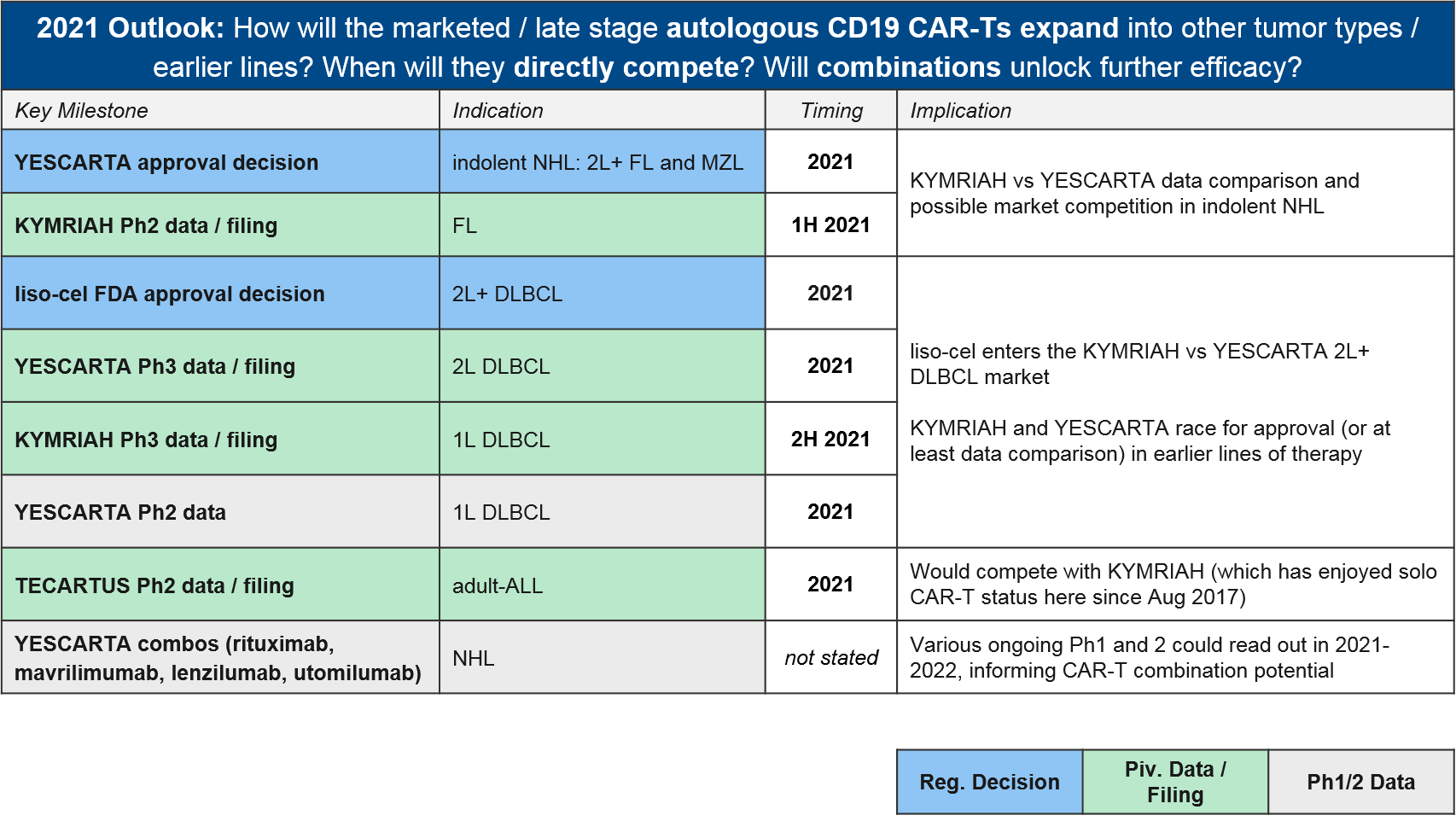

To-date, Gilead’s YESCARTA enjoys a lead in earned revenue, however, things will heat up in 2021 if BMS’ liso-cel does receive FDA approval in 2L+ DLBCL where it would compete with both KYMRIAH and YESCARTA. Meanwhile, the KYMRIAH vs YESCARTA competition will move into earlier lines of therapy. YESCARTA will have a Ph3 readout and possible filing for 2L DLBCL as well as a Ph2 readout for 1L DLBCL. KYMRIAH will have a Ph3 readout and possible filing for 1L DLBCL. In 2021 they will compete in indolent NHL / FL as well. YESCARTA has received a priority FDA review for r/r FL and KYMRIAH has announced a 1H21 Ph2 readout and possible filing in the same indication. In the meantime, Gilead’s TECARTUS (same product as YESCARTA but with an additional manufacturing step) is aiming for a 2021 filing in adult-ALL where it would compete with KYMRIAH.

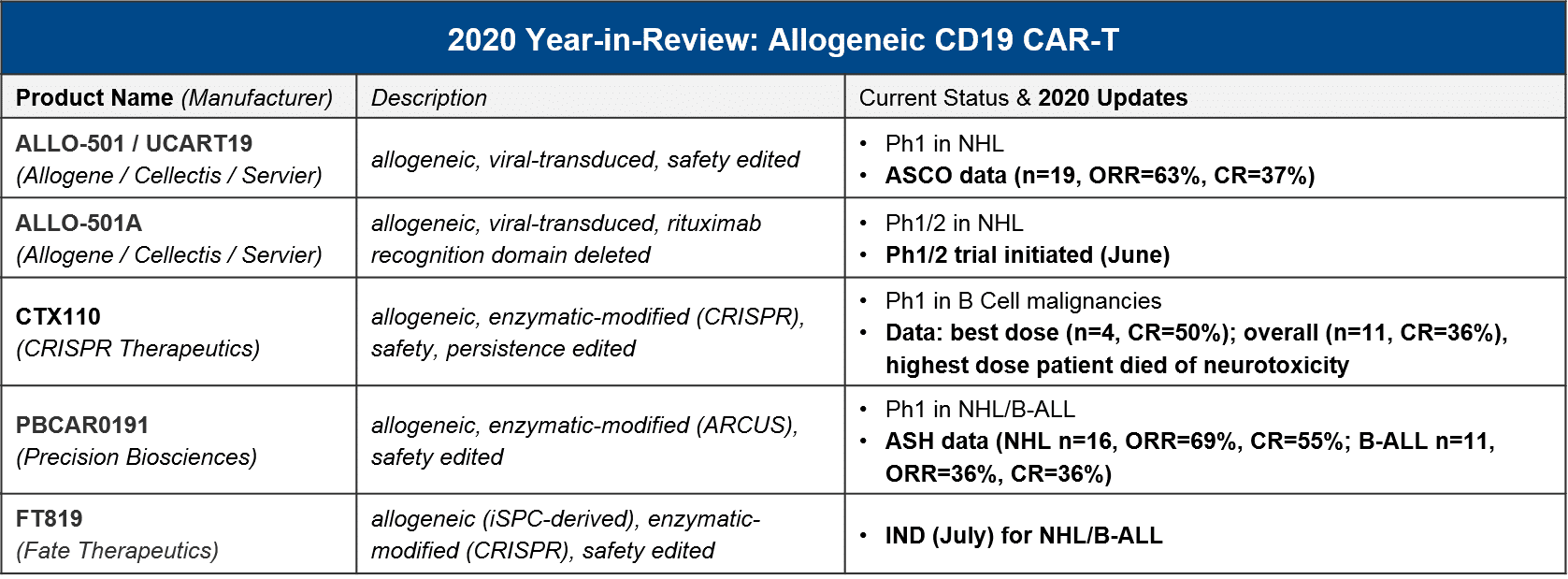

All four of these products are autologous (donor-derived) and modified using viral vectors. One open question has been whether allogeneic products and non-viral gene modifications methods would prove safe, efficacious, and importantly, more feasible and scalable. In 2020 we saw preliminary data that starts to address both of these key questions affirmatively, which has far-reaching implications beyond just the CD19 CAR-T competitive space.

Specifically, in 2020 we saw advancements into clinic as well as early but positive readouts for several allogeneic CD19 CAR-T, three of which are also using enzymatic (non-viral) gene editing technologies:

For context, the registrational trials for KYMRIAH and YESCARTA had ORR=50%/CR=32% and ORR=72%/CR=50%, respectively, with much higher n-values. Taken together, these initial results for the allogeneic / enzymatic gene modified CAR-T, while not clearly superior, are certainly promising given their other product attributes. And very importantly, while there was a patient death from CRISPR’s CTX110 due to immune effector cell-associated neurotoxicity syndrome (ICANS), which is a known AE with other CAR-T cell therapies, there has been no sign of Graft vs Host Disease (GvHD) due to the donor T cells.

While none of these manufacturers have announced dates for future data releases, we expect to see additional interim, and possibly final, Ph1 readouts in 2021, as well as updates on filing timelines based on these complete datasets. It will be particularly informative to see how Fate Therapeutic’s FT819 performs, as it is the first iPSC-derived therapy to enter the clinic. Induced-pluripotent stem cells (iPSC) serve as “master cell lines” which can be maintained over time to offer a standardized, scalable foundation for cell therapy manufacturing. If successful, this approach could streamline and standardize the current patient / donor-derived manufacturing approaches on the market and in the clinic.

BCMA CAR-Ts: which (class of) therapy will take the prize in multiple myeloma?

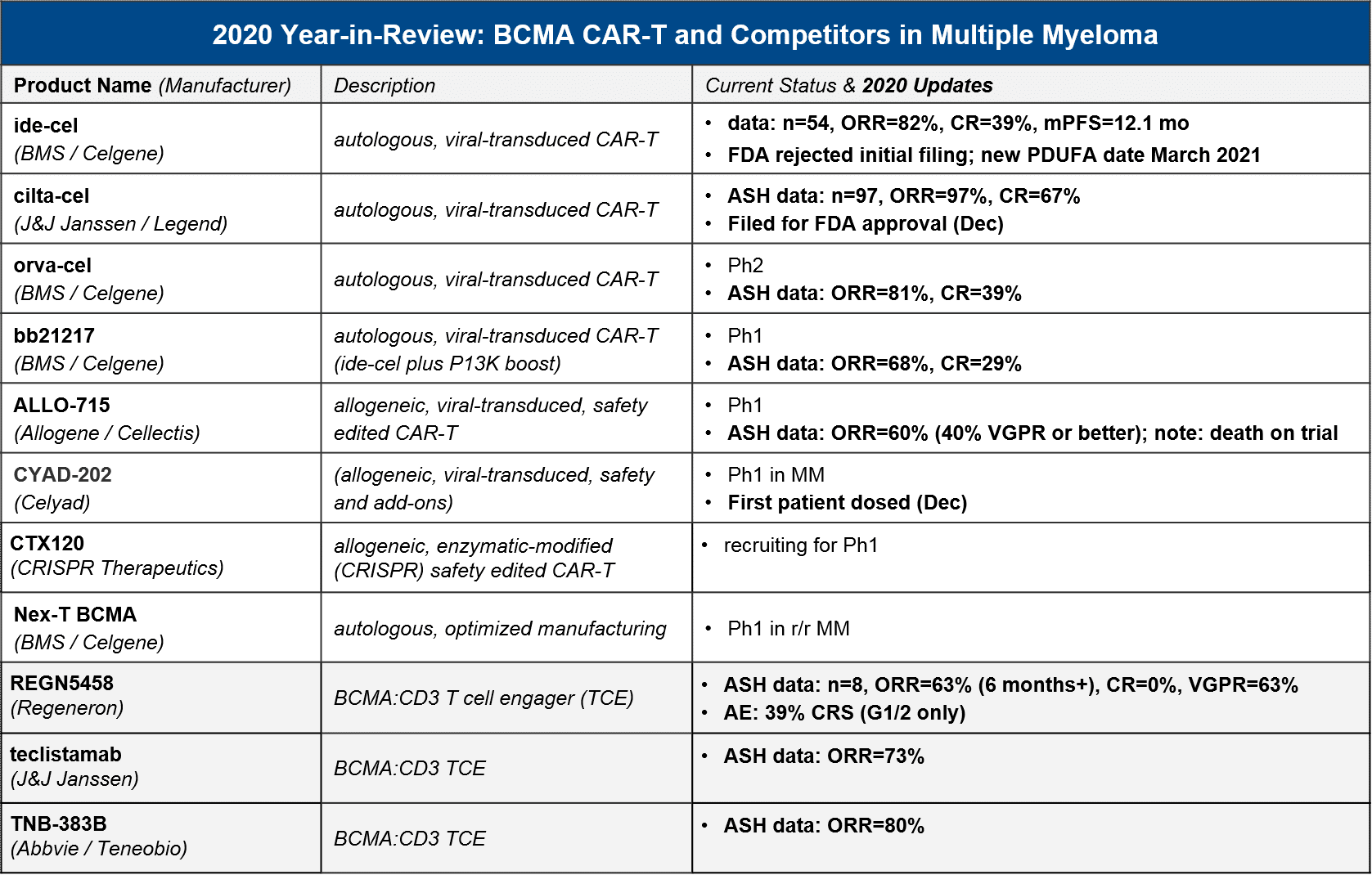

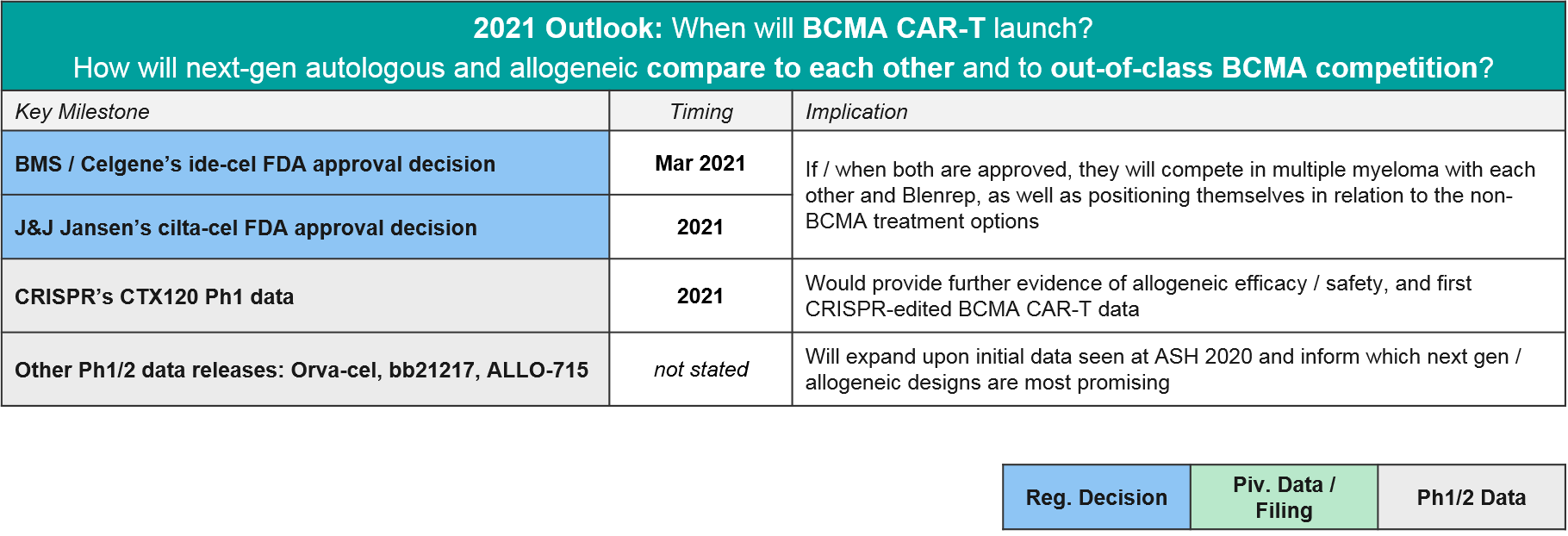

In 2020 the first BCMA targeted therapy in multiple myeloma was approved, GSK’s BCMA-ADC Blenrep (belantamab mafodotin-blmf). BMS / Celgene’s BCMA CAR-T ide-cel was supposed to be hot on their heels, filing for FDA approval in May. However, the FDA unexpectedly refused the filing, citing a need for additional manufacturing information. BMS refiled in July and received a March 2021 PDUFA date, which would have been just in time for their milestone payout (however, liso-cel’s delay has already cost them the payout). In the meantime, competition continues to heat up in the BCMA space – not just within CAR-T including the very impressive data from J&J’s cilta-cel, but also the bispecific T cell engagers (TCE).

In December 2020, there were numerous data releases at ASH which informed several outstanding questions:

- Which autologous CAR-T will take the market lead (once they are approved)? Cilta-cel may launch not far behind ide-cel, with a very impressive ORR and CR

- Can allogeneic compete? Unclear – the only allogeneic data we have to-date is ALLO-715’s relatively modest 60% ORR

- Will bispecific / T cell engagers (TCE) offer a competitive efficacy / safety profile? Possibly, but while the ORR is competitive, we have not seen CR yet, and TCE do have their own serious AEs

For context, GSK’s BCMA-ADC Blenrep was FDA approved based on data showing ORR=31%, 73% with DOR >6 months, n=97, so the CAR-T and TCE both look quite competitive in terms of efficacy. Although some datasets are still early or small, there seems to be a general consensus that the autologous CAR-T have the efficacy edge overall. In particular, J&J / Legend’s “dark horse” contender cilta-cel impressed with a nearly 100% response rate and 67% CR. They filed for FDA approval in December, so in 2021 we may see ide-cel and cilta-cel go head-to-head in the market. While cilta-cel seems to have superior efficacy, it also has greater neurotoxicity, so ide-cel may be able to carve out a niche based on tolerability. The BCMA CAR-T space also has emerging data for “next gen” autologous BCMA CAR-T, namely BMS / Celgene’s orva-cel and bb21217. Orva-cel is one to watch with an impressive 81% ORR and 39% CR. Regarding allogeneic contenders, only Allogene / Cellectis’ ALLO-715 has announced data, with a more modest ORR of 60%.

BCMA CAR-T are not only competing with each other and the approved Blenrep, however. We saw several promising datasets from the TCEs as well, with ORR up to 80%. That said, these data are more preliminary with CR either not announced, or in the case of Regeneron’s REGN5458, none achieved (63% VGPR but no CR).

In 2021 the major BCMA news will be the regulatory decisions for ide-cel and cilta-cel, but we also anticipate maturing datasets in allogeneic CAR-T and TCE that will clarify how the overall BCMA market will play out.

What’s Next for CAR-T Cell Therapies: other targets, technology advances, solid tumors?

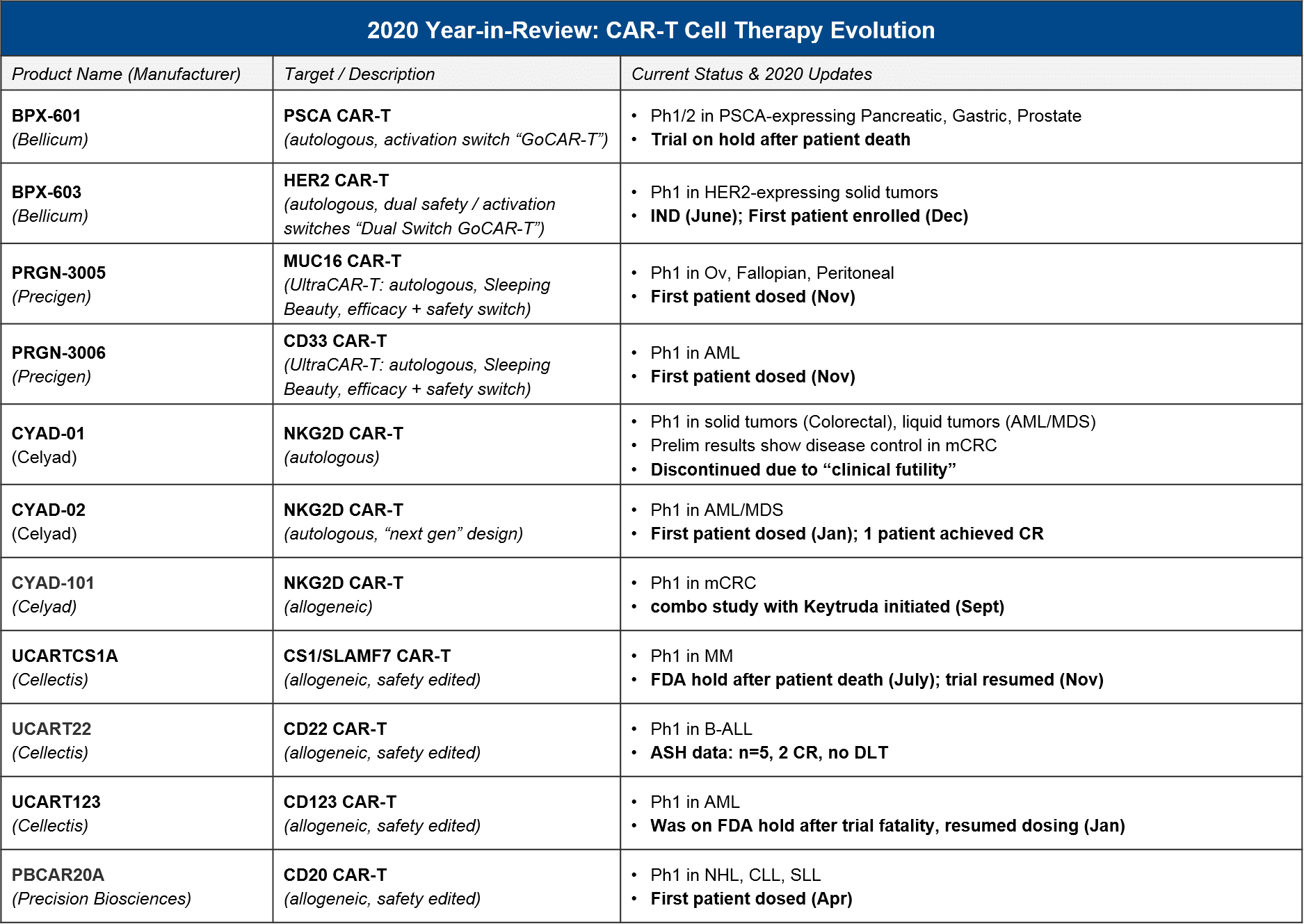

In recent years we have seen many significant advances in the CD19 and BCMA CAR-T spaces, but we also expect additional targets, indications, and designs to reach registrational milestones in 2021-22.

For these earlier stage products, based on their current status, in 2021 we expect preliminary / Ph1 data releases that will inform several key questions about longer-term evolution of T cell therapies, namely:

- How will allogeneic product attributes compare to autologous? See: Celyad, Cellectis, Precision Biosciences platform

- How will non-viral-transduced products compare to viral-transduced? See: Precigen, Precision Biosciences platform

- What other targets will succeed in liquid tumors? Will any succeed in solid? See: PRG-3006, CYAD-02, and Cellectis platform for liquid; all others in solid

- Will safety / activation switches or other modifications boost outcomes? See: BPX-603 and Precigen platform

Non-CAR-T Cell Therapy (TCR-T, TILs, etc) – will we see approval(s) in 2021-22?

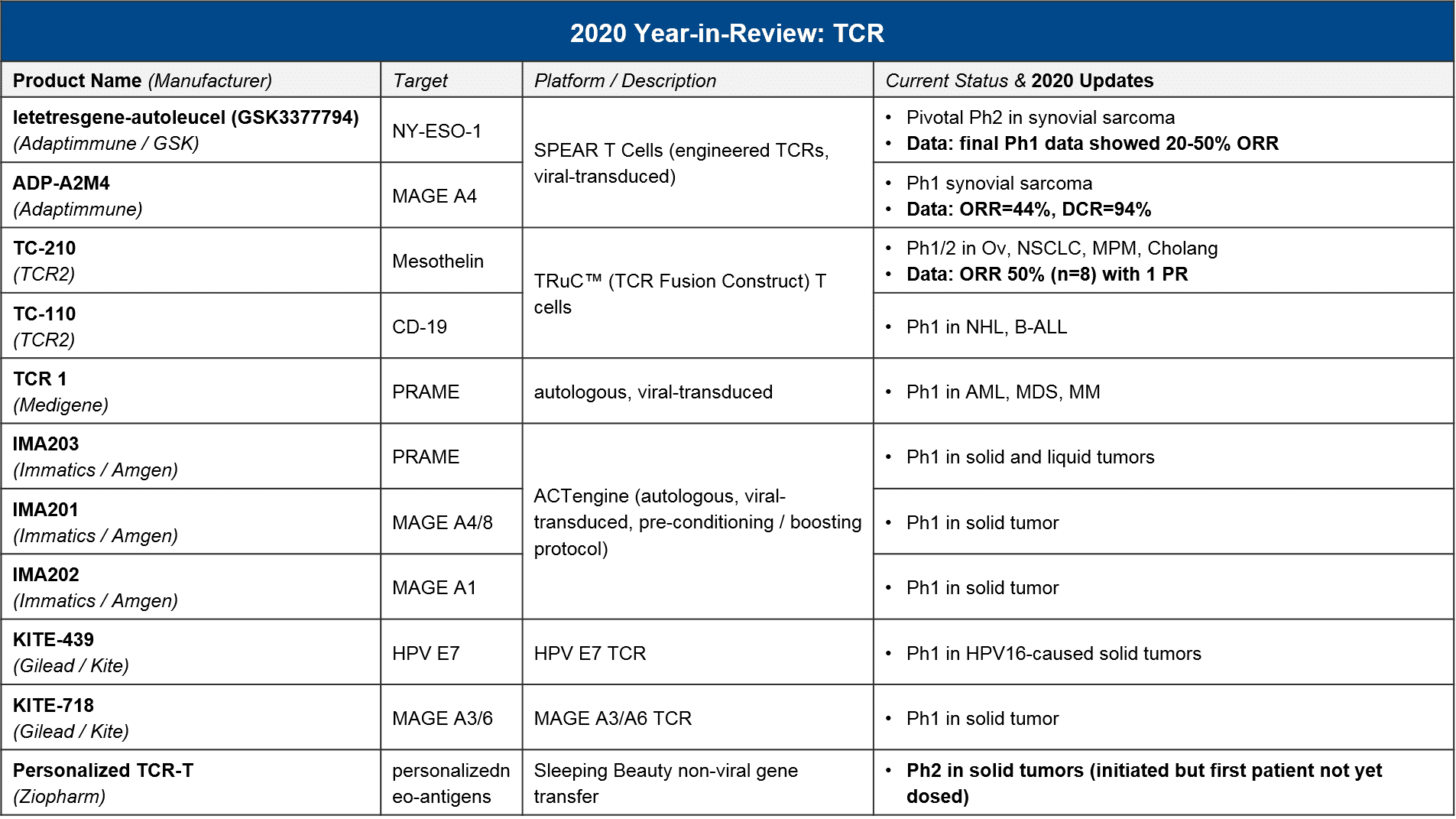

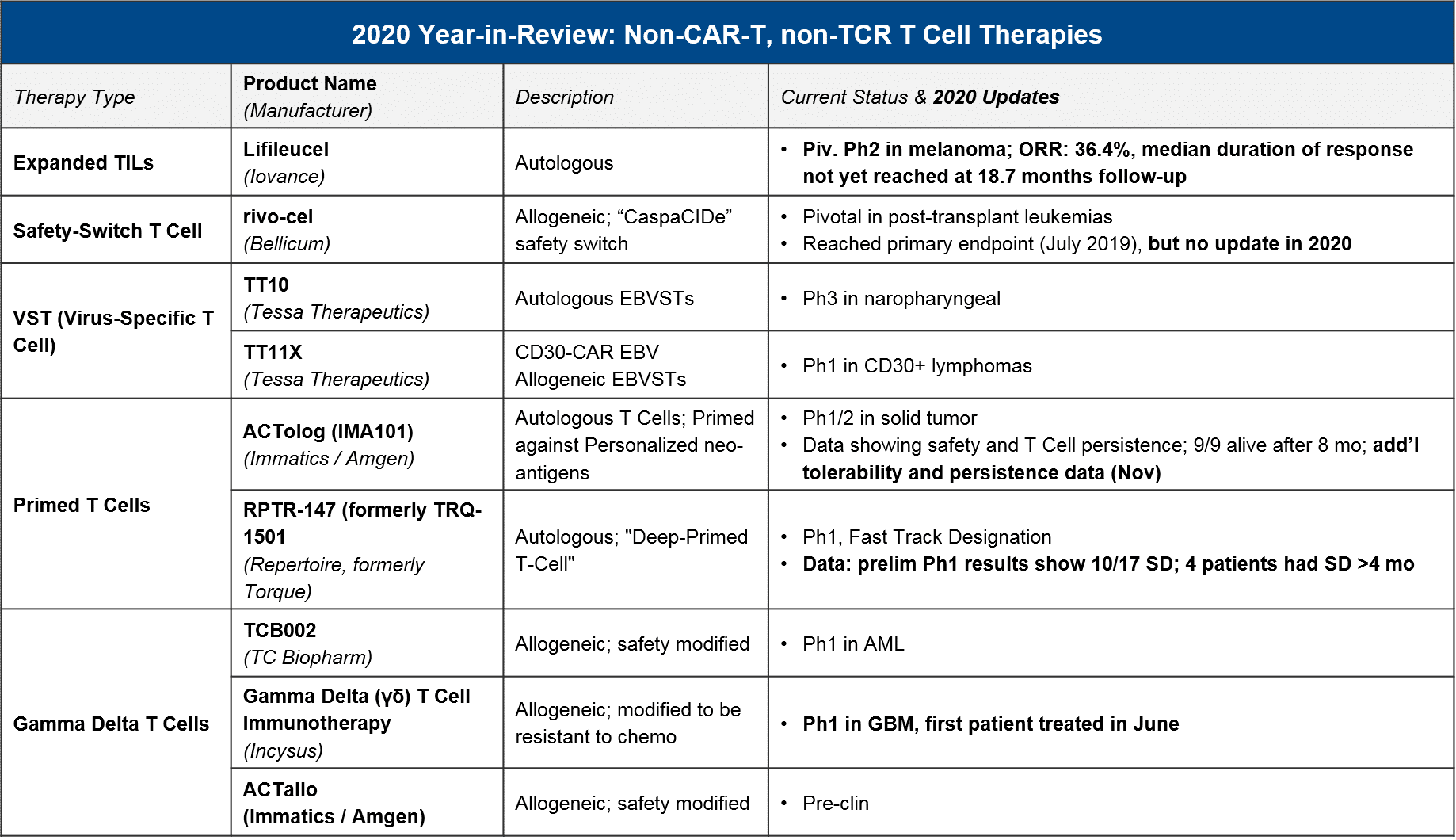

It has been a major question whether and when any of the non-CAR-T cell therapies would successfully file and launch. Here we consider two major categories of non-CAR-T: the first is TCR-T, where the endogenous T cell receptor (TCR) is swapped out for an engineered TCR that will detect a tumor-specific antigen. The key distinction is that CAR-T can only detect tumor-specific antigens that are naturally expressed on the cell surface, whereas TCR-T can detect a tumor-specific antigen that is expressed anywhere within the cell, as long as it is appropriately processed by the MHC cellular machinery. The second category of non-CAR-T is the non-CAR-T, non-TCR-T T cell therapies, which includes purified and reinfused tumor-infiltrating T cells (TILs) as well as safety-edited or otherwise boosted T cells that do not have their T cell receptors modified. Both of these categories are designed to work in solid tumors as well as liquid, although efficacy has been challenging to achieve.

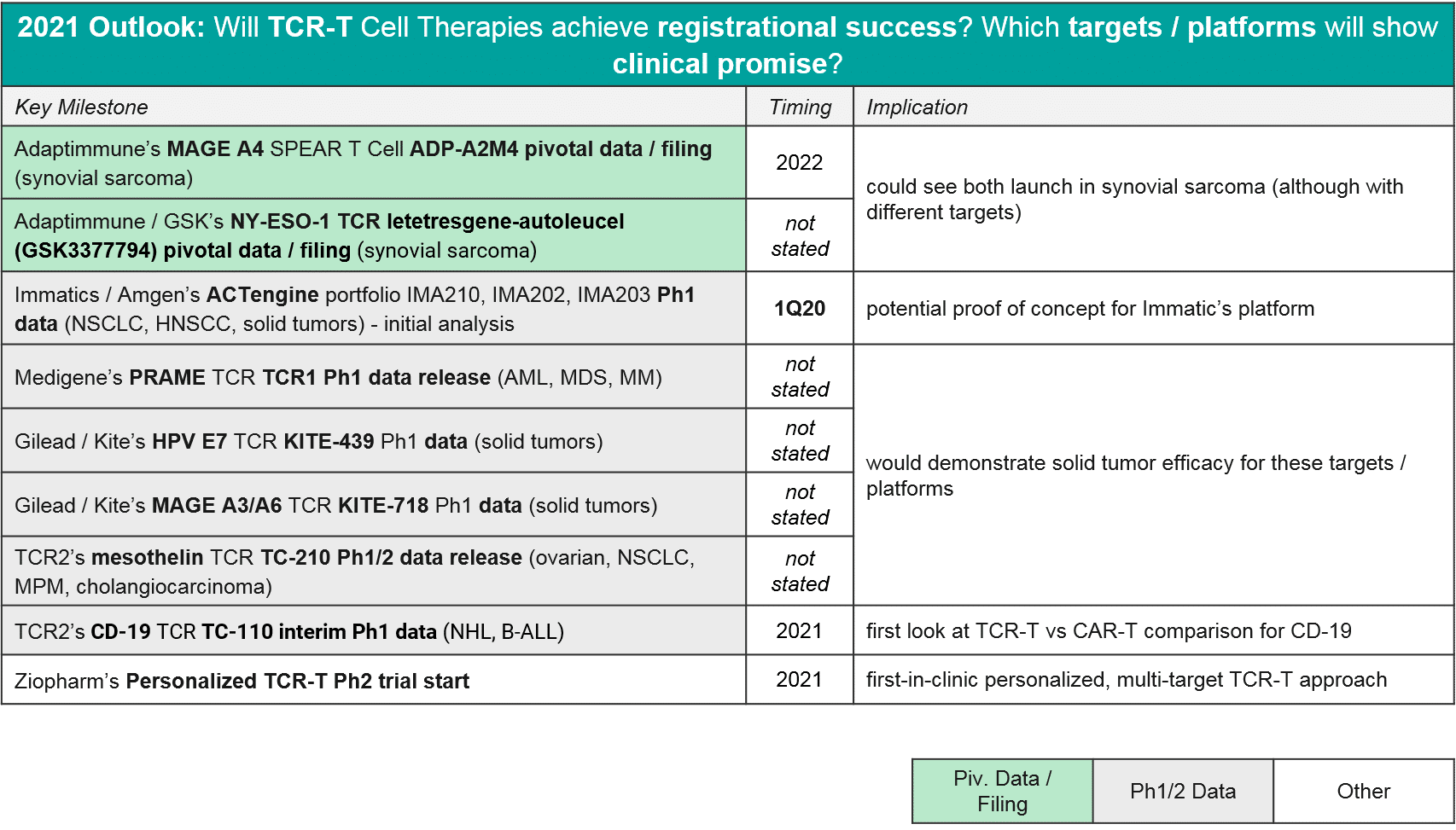

In 2020 there were relatively few data updates for TCR-T, with the key exception of two TCR-T approaching registrational milestones, both in synovial sarcoma. These were GSK / Adaptimmune’s letetresgene-autoleucel, which targets NY-ESO-1 and delivered an ORR=20-50%, and Adaptimmune’s ADP-A2M4, which targets MAGE A4 and delivered an ORR=44% with a DCR of 94%. These are promising data for this difficult to treat cancer, and Adaptimmune has announced they will be filing with an estimated commercial launch in 2022. GSK is likely on a similar timeline, although they have not made a specific announcement. No other TCR-T is in pivotal trial nor has announced timelines for filing or launch, however we expect in 2021 that additional Ph1 datasets will read out and clarify which targets and platforms are most efficacious. As in CAR-T, we expect to see data on a variety of genetic modifications and methods to deliver them (viral vs non-viral), as well as various pre-conditioning and boosting protocols.

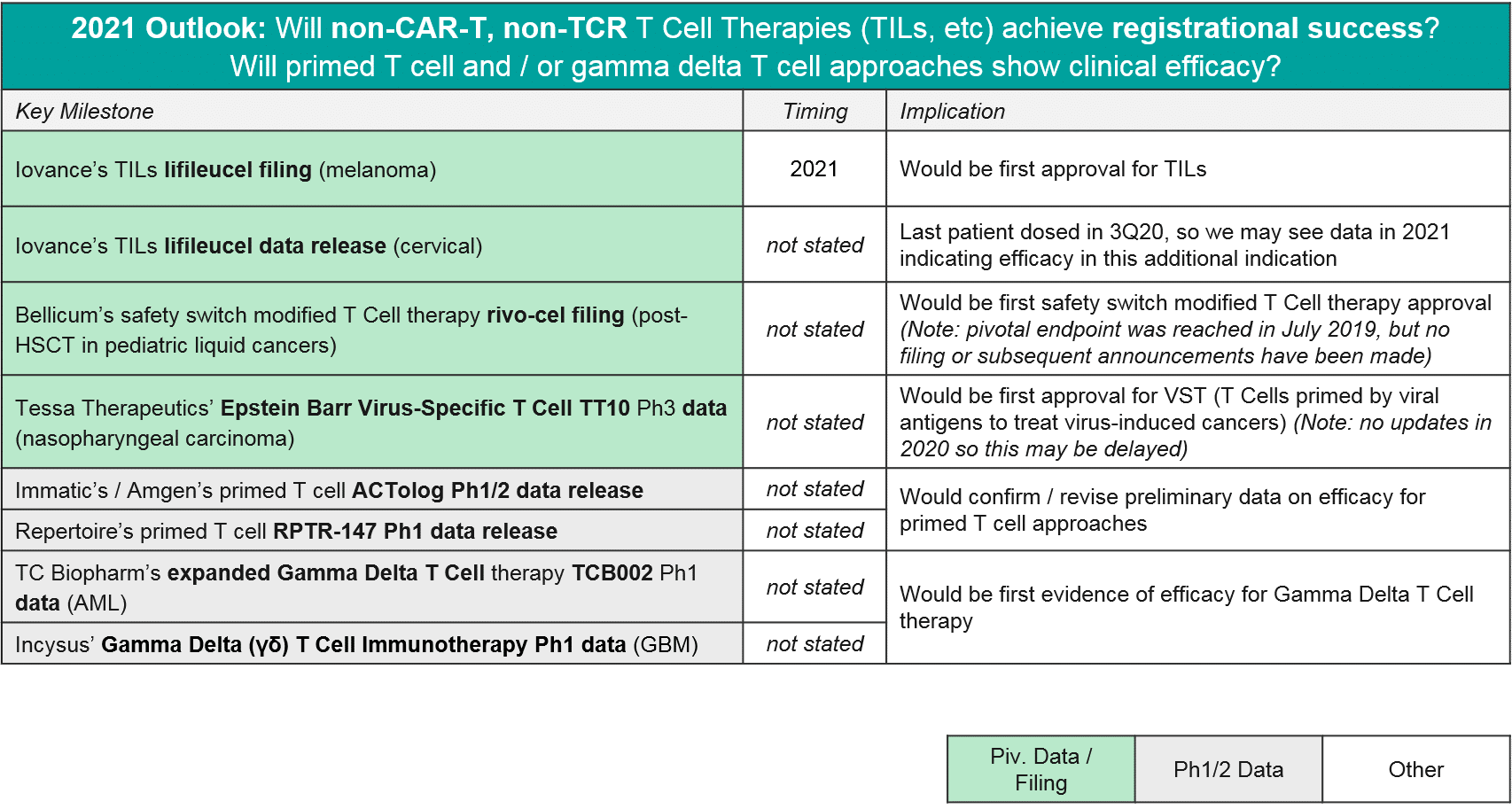

In 2020 we also saw some notable data and registrational progress for non-TCR, non-CAR T cell therapies, in particular TILs. Iovance announced positive pivotal trial data for their TIL therapy lifileucil (LN-145) in heavily-pretreated metastatic melanoma (n=65, DCR=80%, ORR=36%). They plan to file in 2021 and could therefore be the first non-CAR T cell therapy to market. Also in 2020, we saw initial data for primed T cell approaches (Immatics / Amgen’s ACTolog and Repertoire’s TRQ-1501), where T cells are extracted from the patient and then primed against cancer neo-antigens before being re-infused. There is some preliminary evidence of disease control as well as persistence of these T cells over time. And finally, in 2020 we saw additional gamma delta T cells enter the clinic. Gamma delta T cells are a subset of T cells that do not require MHC presentation. So, they could theoretically overcome this known form of tumor resistance without triggering Graft vs Host Disease, which has been a concern with other allogeneic approaches. Therefore, they have good potential as a safe and efficacious T cell-based approach.

In 2021, we expect to see major registrational and clinical updates. Namely, we could see Iovance’s lifileucel filing in melanoma, and perhaps filings (or at least updates) for Bellicum’s rivo-cel in pediatric liquid tumors and / or Tessa Therapeutic’s TT10 in nasopharyngeal carcinoma. Additionally, we may see additional Ph1 data that clarifies the potential of other T cells approaches like primed endogenous T cells (Immatic’s / Amgen’s ACTolog and Repertoire’s RPTR-147) as well as allogeneic gamma delta T cells (TC Biopharm’s TCB002 and Incysus’ in GBM).

Other Cell Therapies: (When) will NK Cells and new DC Vaccines succeed in clinic?

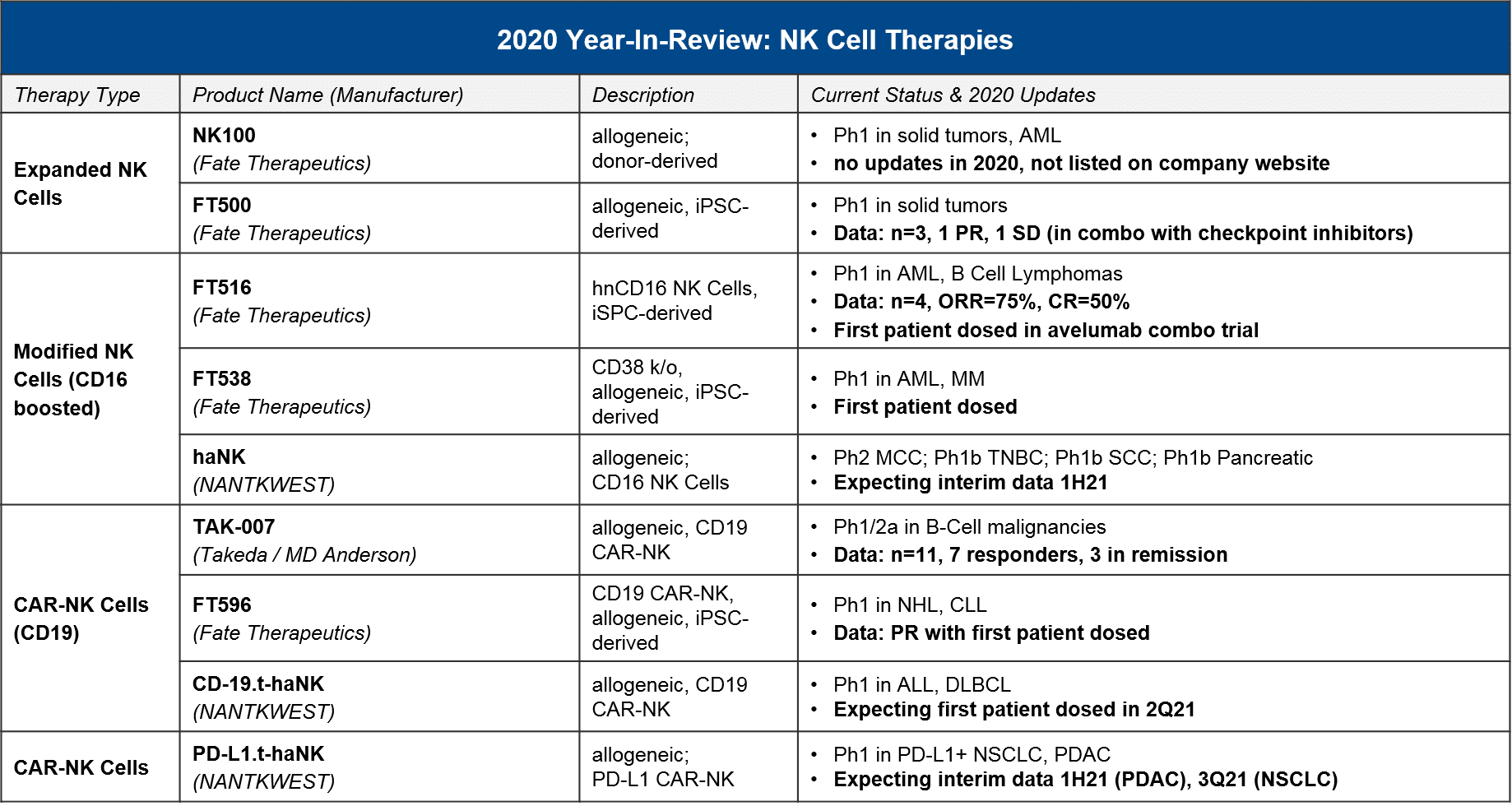

NK cells, which are the cytotoxic effector cells of the innate immune system (as opposed to the adaptive immune system, which is where T cells operate), have long been considered as a promising foundation for cell therapy because they can potentially recognize tumor-specific antigens with less risk of immune “overreaction”. Similar to T cells, there are unmodified, boosted / activated, and CAR-NK iterations under development. In 2020 we saw some very preliminary data, along with further progress into the clinic which should deliver clarifying data in 2021-22.

In 2021, we expect to see further data which characterizes the efficacy and safety of the different NK cell iterations, including CAR-NK for CD19 that can give us a sense of how these therapies will compare to CAR-T.

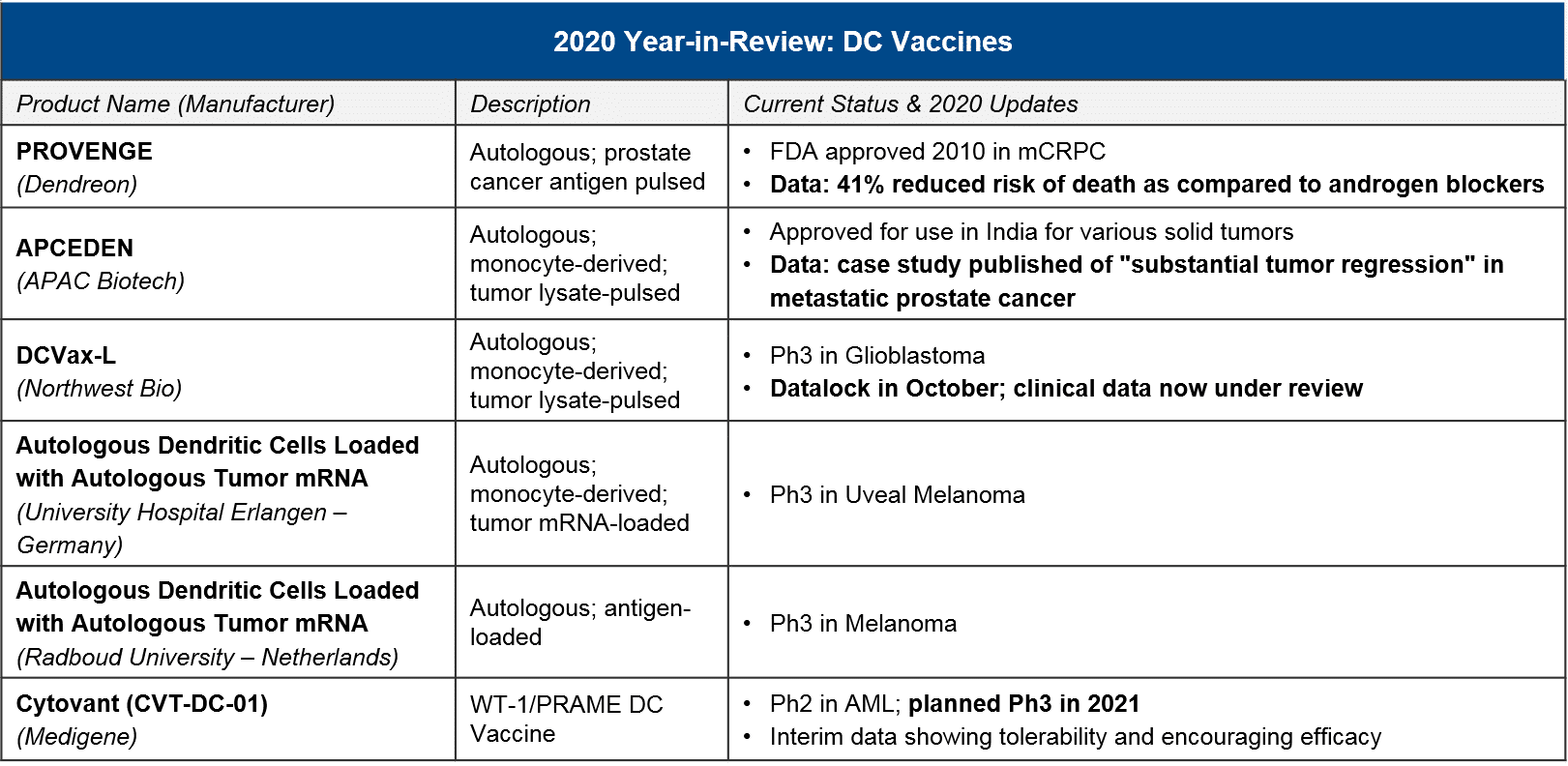

DC “vaccines” are a cell therapy based on Dendritic Cells, which process tumor-specific antigens and activate the adaptive immune system (T cells) to recognize and attack them. For DC vaccines, in 2020 there were no major updates on clinical-stage programs. However, Dendreon’s PROVENGE delivered a new dataset showing a survival benefit over standard of care androgen blockers, and APCEDEN (not approved in the US) published a case study showing a regression. In 2021, we will keep an eye out for Northwest Bio’s Ph3 data release for their DCVax-L in glioblastoma, which had reported promising earlier data on efficacy.

Summary and Conclusions: Looking Ahead to a Competitive 2021

In addition to the specific regulatory milestones and data releases discussed above, in 2021 we will also start to see cell-based therapies position themselves within various competitive markets. While CD19 CAR-T competition will largely be in-class (between established and entering CD19 CAR-T), the BCMA competitive space will be active, not just with out-of-class BCMA therapies like BCMA-ADC and BCMA:CD3 TCEs, but in the context of numerous other multiple myeloma therapies like the CD38 antibodies and other immunomodulating agents. Similarly, for TILs and TCR-Ts trying to break through in melanoma, they must not only demonstrate sufficient efficacy / safety for regulatory approval, they must also carve out a niche amongst numerous established treatments, some of which are already quite effective.

Conversely, there are indications where cell therapies have the potential to offer the first new treatment advances in a long time, for example in synovial sarcoma where two different TCR-T are reaching pivotal stage, and in glioblastoma where a DC vaccine is now undergoing data analysis for a completed Ph3. For both cancers, the current standard of care is surgery plus chemoradiation (with poor outcomes), so there is huge unmet need which cell therapies can hopefully address.

In terms of longer-term out-of-class competition beyond the T Cell Engagers as discussed above, the success of the mRNA vaccine approaches in COVID hints at possible success in cancer as well (where they are being actively developed). However, the early data is mixed at best, with Moderna’s mRNA cancer vaccine mRNA-4157 delivering a ORR of 50% (n=10) in HNSCC, and Roche / BioNTech’s RO7198457 delivering a very low ORR of 8% in their Ph1 trial.

In conclusion, while we did see delays and set-backs in 2020 from COVID-19, namely clinical trial delays and manufacturing issues (which in turn led to regulatory delays), overall the field has made much progress. It has set the stage for an eventful 2021-22 where we expect to see multiple approvals in new targets with the BCMA CAR-T(s) and possibly non-CAR-T therapies as well. In addition, we expect to see data from the numerous Ph1 trials which are continuing to enroll, which will answer questions not just about targets and indications, but about the attributes of allogeneic cell sources, NK cell-based therapies, and various modifications and modification methods (e.g., CRISPR-based). And finally, taken together these data releases and regulatory advancements will further clarify the ultimate potential for cell therapies within the oncology market, including out-of-class competition.